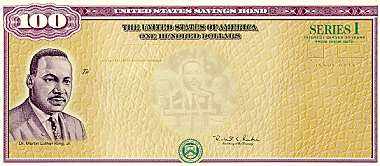

Did you know that Dr. Martin Luther King Jr. is pictured on the Paper Series I $100 Bond?

Now that’s a great bit of trivia to test your kids during Black History Month. I guess it’s not all about the Benjamin’s after all. LOL…a little accountant’s humor interjected there. Okay, let’s get started.

Now that you have a basic understanding of how to make money with bonds and how to pick them based on the two features of quality and duration, we can now advance this discussion to explaining the different types of bonds. The United States Government offers two main classes of bonds – treasury bonds and savings bonds. In this lesson, we will delve into the U.S. Savings Bonds.

Since the government cannot go to a bank and ask for money, when it needs to raise money for wars, deficits, or policy, it has to borrow it from people like you and I. As a result, US backed bonds, like Savings Bonds, are issued to the public when the government needs to raise money.

Education:

On February 1, 1935, President Franklin D. Roosevelt signed legislation that allowed the U.S. Department of the Treasury to sell a new type of security, the U.S. Savings Bond. Since the inception, the U.S. Savings Bond has evolved in form and function. The bonds are now offered in a variety of denominations, including $25 (Series EE), $50, $100, $500, $1,000, $5,000, and $10,000. Besides denomination, the bonds are also offered in different series with varying benefits and restrictions. The table below shows the different series which are still in effect.

|

Series |

Description |

|

E |

No longer available – replaced by Series EE. If owned, they can still be redeemed. The Series E bond was known as the War Bond. |

|

EE |

To help Americans finance their dream of a college education, Congress created the Education Savings Bond program. Under this program, Series EE Savings Bonds purchased by qualified taxpayers on or after January 1, 1990, are tax-free if used to pay tuition and fees at eligible educational institutions. |

|

H |

H Bonds offered a current income bond that paid interest every six months — and earned interest for 30 years. They were replaced by Series HH Savings Bonds in January 1980. |

|

HH |

No longer being issued by the US Government. |

|

I |

The Treasury Department introduced the Series I Savings Bond to encourage more Americans to save for the future while protecting their savings against inflation. The new bond series, launched at an official ceremony led by Vice President Al Gore, is indexed to the Consumer Price Index in denominations as small as $50. |

How US Savings Bonds Work:

Remember the television game show, Let’s make a deal? Well, let’s play.

The Offer:

Uncle Sam approaches you and indicates that he will give you $50 on 2/12/44, if you let him borrow $25 today 2/12/14.

Why would you even entertain such an offer? The answer is – INTEREST!

Uncle sam is offering you this deal because he needs your money today. Since money isn’t free and you worked hard for it, he must compensate you while you are waiting to collect your $50. This compensation comes in the form of interest. He must pay you interest while you hold the bond to maturity or 2/12/44 in this example. The trick is that you will only receive the $50 if you agree to collect on 2/12/44 and not a day before. If you demand your money before that date, then you will not receive $50, you would receive some smaller amount between the original $25 that you loaned and the $50.

That’s it. Would you accept? Before you answer that, let’s examine some of the advantages and disadvantages of U.S. Savings Bond.

Advantages of U.S. Savings Bond

- Safe, risk-free investment

- Endorsed by the U.S. Government

- Multiple denominations are available (from $25 to $10,000)

- Income Tax-free (state and local)

- Certain bonds can be redeemed after a short period of time

- Interest generally compound monthly

- Tax benefits may be available when you use the money for higher education

- Series I bonds may be purchased with your income tax refund

- Electronic bonds are now available – no longer are they only offered in paper

- Some employers allow you to purchase them through payroll deductions

- Great for retirement – buy now and cash them in your retirement years

- Interest on Series HH Bonds are paid in cash

Disadvantages of U.S. Savings Bonds

- Extremely low interest rate

- Highest bond denomination available is $10,000

- Not easily transferrable

- Non-negotiable

- Interest penalty for early redemption

- Meant to be long-term investment (up to 30 years to receive full face value)

- Interest may be subject to federal income tax

- Interest may be included in the value of the bond (Series I and Series EE) – this means that the interest earned will NOT be paid to you in cash.

Resources:

Treasury Direct (www.treasurydirect.gov) – TreasuryDirect is the first and only financial services website that lets you buy and redeem securities directly from the U.S. Department of the Treasury in paperless electronic form. The website offers product information and research across the entire line of Treasury securities, from Series EE Savings Bonds to Treasury Notes. Our TreasuryDirect accounts offer Treasury Bills, Notes, Bonds, Inflation-Protected Securities (TIPS), and Series I and EE Savings Bonds in electronic form in one convenient account.

Important terms from this lesson:

|

Term |

Definition |

| Savings Bond | A U.S. government savings bond that offers a fixed rate of interest over a fixed period of time. |

| Redemption | The return of an investor’s principal in a fixed income security. |

| Redemption Value | Is the price at which the issuing company may choose to repurchase a security before its maturity date. |

Action Step: Replace a kid’s gift with a United States Savings Bond.

Click the link to watch the demo to see how to buy a Savings Bond as a gift http://www.treasurydirect.gov/indiv/planning/plan_giftsdemo.htm