Each Saturday, I will find ways to encourage you to reach your goals. Whether it’s a video, an inspirational message, a poem, or whatever…I want to keep you focused on achieving your goals. Remember that you are the sun and you will provide the light for the people around you to believe. By embarking on this journey, you have already proven that you are a standout in the crowd, a leader. You have shown the desire and willingness to improve your life by implementing new strategies and lessons. I strongly believe that you will be the catalyst for a seismic shift in your family.

Today, our encouragement comes from Vanguard chairman and CEO Bill McNabb and the Five-Minute Rule of Investing

“I believe the children are our future. Teach them well and let them lead the way.” – Whitney Houston

If you remember, the idea of this blog was originally conceived when a child called into the Suzy Orman show. If you don’t recall, then go back to my very first post and read where the inspiration originated.

I have been providing lessons to you each day in an effort to raise your level of financial literacy. Yesterday, it dawned on me that these lessons are not isolated for adults, but are more effective when taught to children because as the song lyrics go, “they are the future, teach then well and let them lead the way.” With that said, each Friday’s lesson from today forth will be to teach financial principles for kids. However, I’m depending on you, parents, to share this information with them. Make financial literacy a priority in your household.

Let’s begin from the beginning – teach your child how to save!

Education:

Let’s face it, kids like to spend money! I don’t think there is a parent who would disagree with that sentiment. The problem is that kids are taught to spend because they are constantly inundated with commercials and advertising campaigns designed to excite the dollars right out of their parent’s pockets and pocketbooks. I don’t blame the kids, heck…they are just being kids…I blame YOU! Yes, you the parents, because many of you have never taught them to SAVE –solvency through appreciating assets of value in my estate.

S – Solvency

A – Assets

V – Value

E – Estate

Teach you child that COINS are there friends! If they learn to associate a simple coin with money in the bank, that association will help them to develop a lifestyle of saving!

What are you teaching your child or children about money? Are you teaching them negative or positive aspects of money? How are your reinforcing their understanding of money? These are questions that you need to ask yourself. If you don’t like the answer, then I challenge you to take advantage of Financial Literacy Friday for Kids!

Resources:

Kids’ Money (http://kidsmoney.org/) – Kids’ Money is an interactive resource for parents, teachers, teens, kids, organizations and international visitors designed to help children develop successful money management habits and become financially responsible adults.

Important terms from this lesson:

Term

Definition

Solvency

In kids’ terms – Having more money and assets than debts!

Estate

In kids’ terms – Everything that you own of value.

Action Step: Make SAVING fun and for a purpose! Here are your instructions.

Buy your child or children a PIGGY BANK. Yes, a piggy bank!

Buy your child a calendar.

Discuss what it means to SAVE with your child – Solvency through appreciating Assets of Value of my Estate.

For 2014, circle one day in the calendar every month so that you have 11 days circled (sinced we are already in the month of February) – this is your official TAKE A KID TO THE BANK DAY.

Find a bank like TD Bank with a penny arcade.

Every month on TAKE A KID TO THE BANK DAY, have your child go to the penny arcade and deposit every coin that they found, earned, or raised during the month. When you get your deposit receipt, use it to open up a SAVINGS (what else) account for your kid.

Repeat this step every month. Once received, go over the receipts with your child so that they can understand how money is saved.

If you have a teenager, then no worries. Just skip the piggy bank portion, but follow everything else. They need to know that one day of the month is set aside to SAVE!

“To improve is to change. To perfect is to change often.” – House of Cards

In the last lesson, we began our introduction to Exchange Traded Funds. While Lesson #30 got the proverbial ETF ball rolling, there was just too much information to fit into one lesson. So, today we will continue exploring the world of ETFs. ETFs are gamechangers! If you want to be an effective investor, then you have to change your approach to investing. The old way of thinking would suggest that if you like Apple, then buy a lot of Apple stock. Well, that’s great if you can afford it. However, we learned in Lesson #16, that Apple stock was trading for about $500 per share. In Lesson #15, I taught you that you never want to put all of your eggs in one basket. Well, that was true, sort of…

ETFs allow you to bet as if you own the entire basket of eggs, even if in reality, you would only be able to invest in one egg. Said another way, ETFs magnify your ability to generate a posItive returns over the long-term.

Education:

In this lesson, we will get into some of the companies that offer the more popular ETFs that are available to investors like you. Since we learned that ETFs trade on stock exchanges just like stocks, there is a plethora of information to help you select the best investment option to fit your specific profile. The most popular ETF Rankings are in the following categories;

Large-Cap

Municipal Debt

China Region

Gold Oriented

Small-Cap

Corporate Debt

Emerging Markets

Commodities

Natural Resources

Real Estate

As you can surmise from the table, ETFs provide great investment flexibility. While you wouldn’t know which stock to invest in a Chinese company, a China Region ETF would enable you to invest in many Chinese companies all at once.

Remember that ETFs are best suited for long-term investors seeking low-cost, diversified portfolios.

Some of more popular ETFs are provided from the following firms who offer many options for investors.

Vanguard

Powershares

Ishares

SPDR (Spider)

MAGNIFY YOUR INVESTMENT RESULTS!

Resources:

SPDR University (http://spdru.com/) – SPDR University (SPDR U) provides online education built exclusively for investment professionals.

Important terms from this lesson:

Term

Definition

PowerShares

PowerShares is an investment boutique firm based near Chicago which manages a family of exchange-traded funds or ETFs marketed by Invesco.

IShares

iShares are a family of exchange-traded funds (ETFs) managed by BlackRock. Each iShares fund tracks a bond or stock market index.

SPDR

SPDR funds are a family of exchange-traded funds (ETFs) traded in the United States, Europe, and Asia-Pacific and managed by State Street Global Advisors (SSgA). Informally, they are also known as Spyders or Spiders.

Action Step: Let’s go back to college with SPDR University.

Go to SPDR University and view the online courses to learn more about ETFs.

You may know your ABCs, but do you know your ETFs?

The above image depicts a favorite dish from my youth, alphabet soup. Have you ever heard of S&P, NYSE, NASDAQ or FTSE? A better question may be, do you understand what these acronyms mean?

In the world of investing, it can often feel like you are in stuck in a bowl of alphabet soup. When most people see these titles, they are understandably intimidated. In this lesson, I will provide an introduction to Exchange-Traded Funds (ETFs) and discuss how they can be used to help you reach your investment goals.

Education:

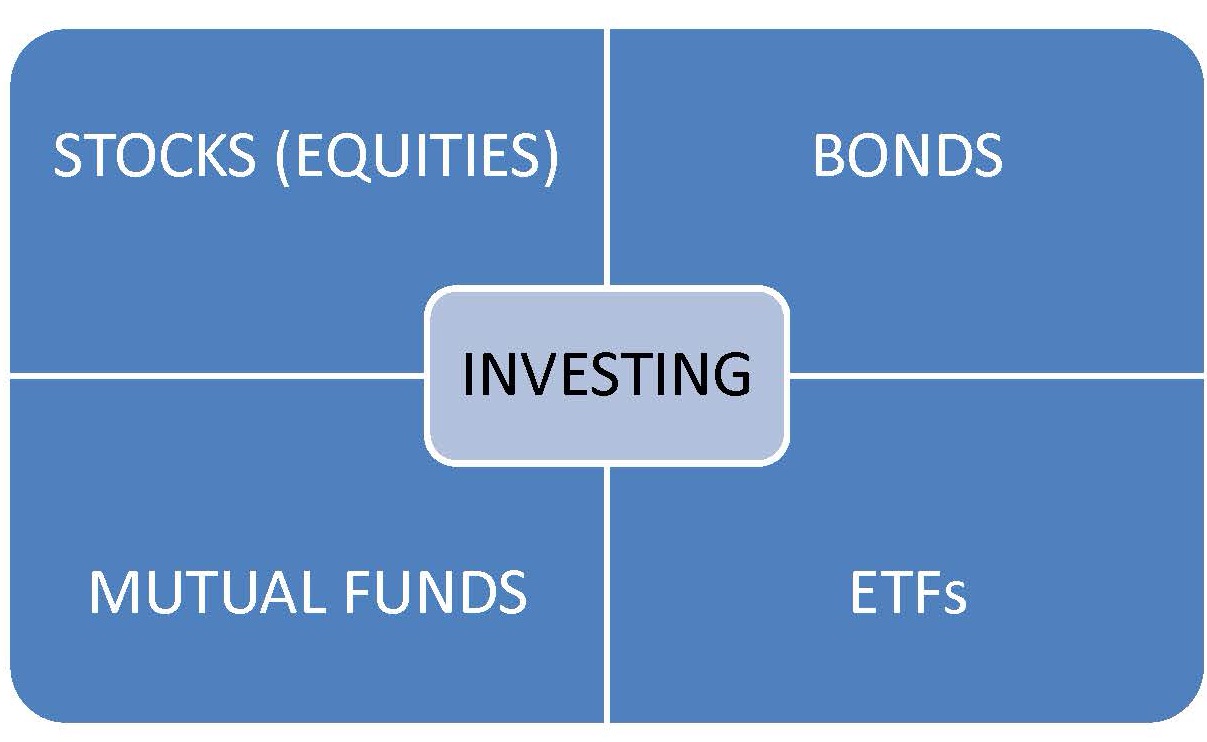

The last category in the investing diagram is ETFs or Exchange Traded Funds.

An exchange-traded fund (ETF) is an investment fund traded on stock exchanges, much like stocks. An ETF holds assets such as stocks, commodities, or bonds. Most ETFs track an index, such as a stock index or bond index. The purpose of an ETF is to match a particular market index. Because, technically, you cannot actually invest in an index, exchange-traded funds allow investors to invest in securities which seek to replicate the index.

In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of the market. Indexes can be based on various categories of stocks. There are the widely known market indexes, such as the Dow Jones Industrial Average, the NASDAQ Composite, or the S&P 500. The Standard & Poor’s 500 (aka S&P 500) is one of the world’s best known indexes, and is the most commonly used benchmark for the stock market. The S&P 500 is a stock market index based on the market capitalizations of 500 large companies having common stock listed on the NYSE or NASDAQ.

When you buy shares of an ETF (e.g. Vanguard S&P 500), you are buying shares of a portfolio that tracks the yield and return of its native index, or the S&P 500 in this instance. Although the Vanguard fund was an example of overall stock market index, there are indexes based on market sectors, such as tech, healthcare, financial; foreign markets; market cap (micro-, small-, mid-, large-, and mega-cap); asset type (small growth, large growth, etc.); even commodities. ETFs provide great flexibility for niche investors.

Benefits of ETFs

ETFs combine the range of a diversified portfolio with the simplicity of trading a single stock.

Investors can purchase ETF shares on margin, short sell shares, or hold for the long term.

Passive management, fund or money manager makes only minor, periodic adjustments to keep the fund in line with its index.

ETFs mitigate the element of “managerial risk” that can make choosing the right fund difficult.

ETFs allows you to harness the power of the market itself.

Fewer administrative costs than actively managed portfolios.

Tax efficiency – fewer taxable distributions.

Highly efficient investment

Diversification

High liquidity – enabling investors to get into and out of investment positions with minimum risk and expense.

ETF shares trade exactly like stocks.

Resources:

CNN Money ETF Finder (http://bit.ly/1oTHzJH) – provides a tool to help investors find funds to fit their individual criteria.

The Vanguard S&P 500 fund – The Fund is a low cost way to gain diversified exposure to the U.S. equity market. The fund invests in 500 of the largest U.S. companies, which span many different industries and account for about three-fourths of the U.S. stock market’s value

“Life is like a box of chocolates, you never know what you’re gonna get. “ –Forrest Gump Eureka! Forrest Gump was on to something when he uttered one of the most famous movie quotes in history.

On Friday, we celebrated Valentine’s Day and I commemorated the occasion by giving my partner a large heart-shaped box of chocolates. Because the box was so large, four days later, we are still enjoying those bite-sized edible rays of joy. Upon removing the lid, all that is visible to the eye is the shape of the chocolate. Because we lack the x-ray vision of Superman, the only way to know what is on the inside of the chocolate, the filling (e.g. nougat, almonds, caramel, etc.) is to examine the map that is included in the box, a cheat sheet of sorts which tells you exactly what is in each chocolate. Although they appear similar to the naked eye, each chocolate has its own characteristics. Some are made of dark chocolate, some of milk chocolate, some contain nuts, some do not and so on. Using this map, my partner knew to steer clear of caramel because she hates it. However, I love caramel, so I used the map to zero in on my favorite filling.

If I can take a few liberties with Mr. Gump’s quote, I would say that Mutual Funds are like a box of chocolates, however, the map tells you exactly what you are going to get. In the world of mutual funds, this map is called a prospectus.

Education:

In Lesson #28, we began our discussion of mutual funds and how they can be used to give a small investor the purchasing power or wherewithal of a large investor. In this lesson, we will discuss how to pick the right chocolate!

A prospectus, is the map that teaches what each chocolate contains. It is absolutely critical that you read a prospectus before investing in a mutual fund. Would you eat a chocolate with almonds if you were allergic to nuts? Maybe…if you didn’t know, but would you take the risk? The prospectus gives you all of the information about the mutual fund, including the following.

What shareholder services is available in the fund

Distribution information

Tax information

Fees and expenses *

Performance results

The investment goals of the fund

The investment holdings

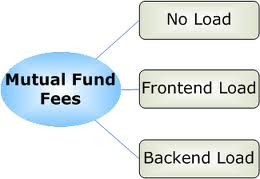

Of the seven items listed above, the most important items to understand are the fees and expenses. For Mutual Funds, so

Load Fees (Front-end, No Load or Backend Load)

Contingent (CDSL)

12b-1 fee

Management Fees

Redemption Fees

Example: If you invest $10 and the investment earns $5, then you would think that you $15, right? Wrong, read the fine print.

Mutual Fund fees can turn your potential $15 into $3 without using magic. BEWARE OF FEES!

ALWAYS READ THE PROSPECTUS!

Resources:

FINRA (http://www.finra.org/ ) – The Financial Industry Regulatory Authority is an independent, not-for-profit organization authorized by Congress to protect America’s investors by making sure the securities industry operates fairly and honestly.

Important terms from this lesson:

Term

Definition

Prospectus

A document that contain the facts that an investor needs to make an informed investment decision.

Front-end Sales Load

A type of fee that investors pay when they purchase fund shares.

No Load Fund

A mutual fund in which shares are sold without a commission or sales charge.

Backend Sales Load

A type of fee that investors pay when they sell fund shares.

Contingent (CDSL) Fees

A type of fee that investors pay only when they redeem fund shares

12b-1 fee

An annual fee paid by the fund for distribution and/or shareholder services

Action Step: Watch the animated video and learn about mutual fund fees.

On May 22, 1980, my life changed when the Pac-Man video game was released. I’m sure you are wondering why I would use an image of Pac-Man to discuss Mutual Funds. Well, the video game provides a great way to demonstrate how Mutual Funds give you PURCHASING POWER. Think of yourself as Pac-man. When the game opened, you were being chased by larger investors who could literally swallow you up. However, if you were able to make it to a power pill, it gave you super powers to chomp up the pellets (investments). Well, mutual funds are your power pill. Without it, most investors are intimidated by the investing landscape; however, with the assistance of a power pill, you could magnify your potential to swallow up investments. Most of us lack the capital resources to invest effectively in large companies. However, when we pool our resources, we have the ability to invest on a large scale.

Education:

In Lesson #15, the INVESTING diagram was used to introduce the most popular investment alternatives for the average investor. Because of the pervasiveness and utility of stocks and bonds, I dedicated two full weeks of lessons to discuss them in greater detail. Because those are the most common investments, it only made sense to begin our focus on those two areas. Today’s lesson will be dedicated to exploring Mutual Funds.

Do you have a 401(k)?

Do you have a 403(b)?

Do you have a 457 plan?

If you answered yes to any of those questions, then either you are an employee or have been an employee of an organization that offered these qualified retirement plan options to you. However, did you know these plans are only able to invest in mutual funds? HMMMM…

If you are astute, then you will notice that I did not ask you if you had an IRA plan. That’s because IRA plans are unqualified plans. What does that mean? It means that they are NOT tax-advantaged plans. Let’s just keep it at that level for now because the mechanics of the IRA plan is not the intention of this lesson. We will table that discussion for another day.

What is a MUTUAL FUND? Let’s analyze this by breaking it down to bit-sized pieces.

Mutual – to hold in common by two or more parties, a pool.

Fund – a source of money that is allocated to a specific purpose.

A mutual fund is an:

Investment vehicle

Consists of a pool of money collected from people (investors) with a common purpose (to invest)

Organized into classes (stocks, bonds, cash)

Operated by money managers who are in charge of the pool

To achieve diversification

Consider this – you and your friends decide that you want to start a fund to invest in small businesses in your area. Is this a mutual fund?

Let’s test our simple definition:

Is it an investment vehicle? Yes

Does it consists of a pool of money collected from people with a common purpose? Yes

Is it organized into classes (stocks, bonds, cash)? Yes

Is it operated by a money manager? Yes, the group

Does it seek to achieve diversification? Yes, it will invest in multiple businesses

Then yes, this is a mutual fund. Of course, that example is quite innocuous, but it’s critical to chop these terms into bit-sized pieces that you can ingest. Now that we have a basic framework, let’s advance the discussion.

Mutual Fund Investment Classes

Equity Fund (invest mostly in stocks)

Large Cap

Mid-cap

Small Cap

Growth

Value

Blend

International

Funds of Funds

And so on…

Bond (invest mostly in bonds)

Government Bonds

Corporate Bonds

Long-term Bonds

Short-term Bonds

Fixed Income (invest in municipal bonds)

As you can see, the mutual fund investment classes can be broken down and targeted to achieve your investment objective. Since most of us do not have the capital or wherewithal of a Warren Buffett or Karl Icahn, who can invest large amounts of money in individual investments, mutual funds give small investors (the majority of us) the ability to pool our resources with other investors to purchase the same type of investments. A mutual fund is formed for PURCHASING POWER. For example, let’s take the tech industry. Within that industry, you may have companies like Microsoft, Apple, Intel, Google. The individual stock prices of all of those companies are extremely expensive. Even if you could buy a few shares, that wouldn’t make a difference. However, if you teamed up with others, then together you would have a large pool of funds to invest in all of these companies.

Advantages of Mutual Funds

Purchasing Power

Plethora of mutual fund classes (can target investments)

Diversification

Experienced Money Manager

Dividend reinvestment (buy more shares)

Some mutual funds offer investors different types of shares

Disadvantages of Mutual Funds

Hidden Fees (BE CAREFUL HERE)

Load vs No load (to be discussed in Lesson #29)

Limited exposure to lone investments (your favorite investment may only represent a small portion of the fund’s holdings)

Unscrupulous money manager

Tax issues (capital gain distributions)

Poor trade execution (may not give you the best price)

Some mutual funds offer investors different types of shares

If you noticed, one item was listed as both an advantage and a disadvantange of mutual fund investing. In the next lesson, we will explore this in greater detail.

An investment program funded by shareholders that trades in diversified holdings and is professionally managed.

Qualified Retirement Plan

A plan that meets requirements of the Internal Revenue Code and as a result, is eligible to receive certain tax benefits. These plans must be for the exclusive benefit of employees or their beneficiaries.

Money Manager

A business or bank responsible for managing the securities portfolio of an individual or institutional investor.

Action Step: Watch the video, An Introduction to Mutual Funds.

Each Saturday, I will find ways to encourage you to reach your goals. Whether it’s a video, an inspirational message, a poem, or whatever…I want to keep you focused on achieving your goals. Remember that you are the sun and you will provide the light for the people around you to believe. By embarking on this journey, you have already proven that you are a standout in the crowd, a leader. You have shown the desire and willingness to improve your life by implementing new strategies and lessons. I strongly believe that you will be the catalyst for a seismic shift in your family.

Today, our encouragement comes from Warren Buffett – How to Turn $40 into $5 Million

Have a beautiful Saturday!

Action Step: Be encouraged and do not forget to pay yourself today!

Given that today is Valentine’s Day, I will be the first to admit that bonds are not the sexiest investment to talk about. However, it is critical that you understand how this fixed income security fits into your overall investment portfolio. First, it provides stability to counterbalance other more risky investments in your portfolio. Even the riskiest people among us, loves a little certainty. This past week was spent demystifying the world of bonds to make it more accessible to you. You may not like bonds now, but if you live long enough, then they will make a great bed fellow in your latter years.

Education:

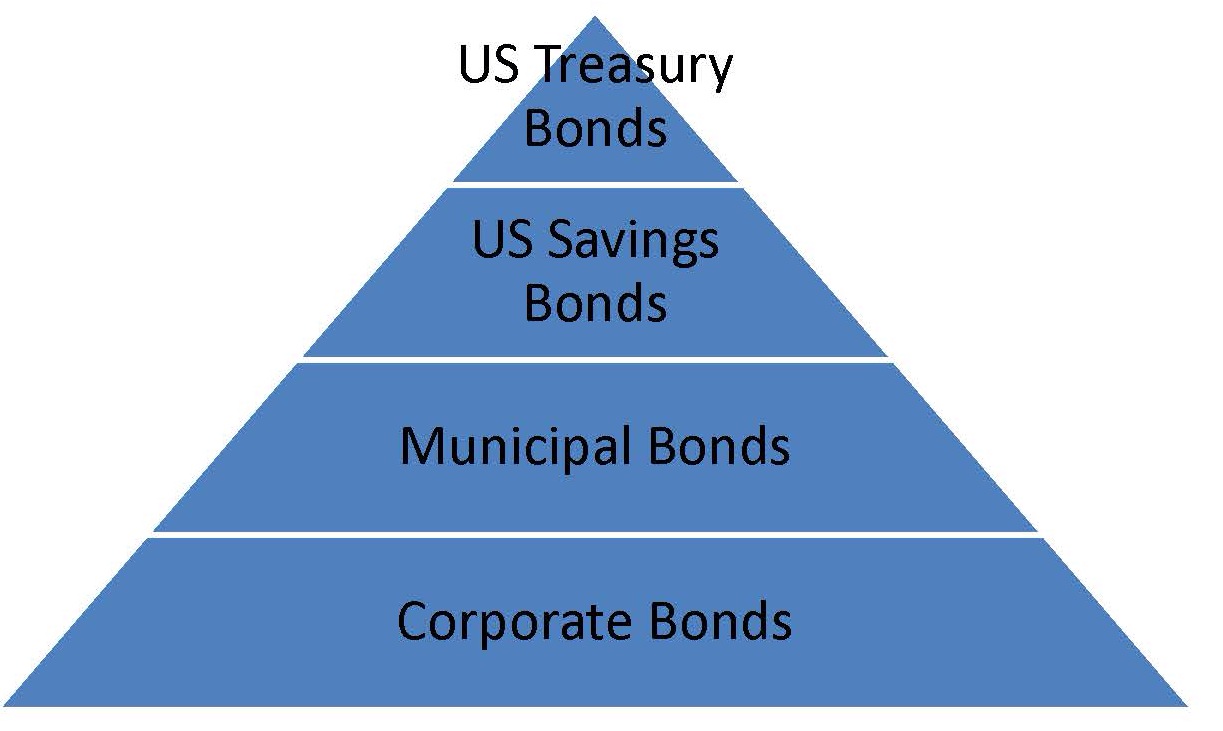

In this lesson, we will close out out the bond pyramid that was introduced in Lesson #22. In case you forgot the hierarchy, let’s take another look.

I dedicated the last two lessons to discussing the benefits of investing with our very own United States Government. It felt good for the government to owe us some money for a chance. As a creditor of the U.S. Government holding either Treasury Securities or Savings Bonds, your money is in good hands. We can now shift our focus to the distant relative of those secure investments – Municipal Bonds and Corporate Bonds.

Municipal Bonds, or Munis are debt securities issued by a state, municipality or county to finance its capital expenditures. Municipal bonds are exempt from federal taxes and from most state and local taxes, especially if you live in the state in which the bond is issued. Municipal bonds may be used to fund expenditures such as the construction of highways, bridges or schools. “Munis” are bought for their favorable tax implications, and are popular with people in high income tax brackets.

The primary reason that people invest in Municipal Bonds is – Tax-exempt interest.

EXAMPLE: If you buy $10,000 worth of municipal bonds with a 4% coupon, the $400 you receive every year is tax-free. Kaboom! Anytime you can earn tax-free income, that’s a Kaboom!

Corporate Bonds are debt securities issued by a corporation and sold to investors. The backing for the bond is usually the payment ability of the company, which is typically money to be earned from future operations. In some cases, the company’s physical assets may be used as collateral for bonds. Corporate bonds are considered higher risk than government bonds. As a result, interest rates are almost always higher, even for top-flight credit quality companies.

The primary reason that people invest in Corporate Bonds is – Higher Interest Rates.

EXAMPLE: If you buy $10,000 worth of municipal bonds with a 4% coupon, you will receive $400 in interest. However, if you buy $10,000 worth of corporate bonds with a 6% coupon, you will receive $600 in interest.

It’s not rocket science. You are simply looking for the angel which will earn you more money. That’s it!

While those definitions provide a conceptual framework, bonds are quite complicated and these lessons serve only to introduce these investment alternatives to you. You certainly do not want to attempt to invest in Municipal or Corporate Bonds without a sound financial advisor (refer to Lesson #18).

Here’s a joke. A bill, a note and a bond walk into a bar. Who leaves first?

At the end of this lesson, you will be able to answer that question.

Education:

In the last lesson, we introduced the U.S. Savings Bonds. Today, we will discuss the other investment alternative offered by the United States Government – U.S. Treasury Securities.

U.S. Treasury Securities come in three different classes based on their length to maturity.

Class #1 – U.S. Treasury Bills (maturities range from a few days to 52 weeks)

Class #2 – U.S. Treasury Notes (maturities of 2, 3, 5, 7 and 10 years)

Class #3 – U.S. Treasury Bonds (matures in 30 years)

Treasury Bills

Treasury bills, or T-Bills mature in one year or less, they do not pay interest prior to maturity; instead, they are sold at a discount of the par value to create a positive yield to maturity or profit for the investor.

For instance, you might pay $990 for a $1,000 bill. When the bill matures, you would be paid $1,000. The difference between the purchase price and face value is profit.

Treasury Notes

Treasury Notes, or T-Notes mature in two to ten years, pays interest every six months, and have denominations of $1,000. In the basic transaction, one buys a “$1,000” T-Note for say, $950, collects interest over 10 years of say, 3% per year, which comes to $30 yearly, and at the end of the 10 years cashes it in for $1000. So, $950 over the course of 10 years becomes $1300.

Treasury Bonds

Treasury bonds mature more than ten years (up to 30 year). Treasury bonds pay a fixed rate of interest every six months until they mature. When a bond matures, the owner is paid the face value of the bond. Bonds can be held until maturity or sold before maturity.

Let’s recap:

Type of Security

Maturity

Pays Interest

Treasury Bills (T-Bills)

Less than 1 year

No

Treasury Notes (T-Notes)

2 – 10 years

Yes, every 6 months

Treasury Bonds

More than 10 years

Yes, every 6 months

Advantages of U.S. Treasury Bond

Safe, risk-free investment

Backed by the full faith and credit of the U.S. Government

Purchased directly from the U.S. Treasury in $100 increments

Pays a fixed amount of interest (based on the discount rate)

Interest earned is exempt from state and local income tax

Great for retirement

T-bills and T-Notes are great short term investments

Diversify your investment portfolio

T-Bills can be purchased in virtually every type of investment account, including Coverdell ESA’s, UTMA/UGMA custodial accounts, and educational trusts. Additionally, many Section 529 plans offer a low-risk mutual fund option that is heavily invested in T-Bills.

Disadvantages of U.S. Savings Bonds

Interest rate varies with maturity of security – still comparatively low based on other types of investments

High purchase limit (up to $5 million)

Interest earned is subject to federal income tax

Opportunity Costs of money tied up especially in Notes and Bonds

Resources:

Treasury Direct (www.treasurydirect.gov) – TreasuryDirect is the first and only financial services website that lets you buy and redeem securities directly from the U.S. Department of the Treasury in paperless electronic form. The website offers product information and research across the entire line of Treasury securities, from Series EE Savings Bonds to Treasury Notes. Our TreasuryDirect accounts offer Treasury Bills, Notes, Bonds, Inflation-Protected Securities (TIPS), and Series I and EE Savings Bonds in electronic form in one convenient account.

Important terms from this lesson:

Term

Definition

Treasury Bills or T-Bills

A bill is a short-term investment issued for a year or less.

Treasury Notes or T-Notes

Are government securities that are issued with maturities of 2, 3, 5, 7, and 10 years and pay interest every six months.

Treasury Bonds

Pay interest every six months and mature in 30 years.

Discount

Means a purchase price that is less than the face value of the security.

Discount Rate

Another name for the coupon or interest rate given to a security.

Opportunity Costs

The cost of an alternative that must be forgone in order to pursue a certain action. Put another way, the benefits you could have received by taking an alternative action.

Action Step: Watch the short video to drive this lesson home.