Let’s Play Financial Soccer Is your financial knowledge ready for a workout?

Word hard, play hard!

Education:

Today’s lesson will test your knowledge of financial information. You have worked hard all week with demanding lessons, so it is time to unwind. Financial Soccer is part of Practical Money Skills for Life (www.practicalmoneyskills.com) a free, award-winning financial education program that reaches millions of people around the world each year.

Practicemoneyskills.com – A website to help consumers and students of all ages learn the essentials of personal finance.

Important terms from this lesson:

Term

Definition

FUN

No definition needed!

Action Step: Download and play the Financial Soccer game.

Today is about having fun, so grab the kids and play Financial Soccer.

Available online at http://www.financialsoccer.com/play puts students’ fiscal knowledge to the test in an online simulation game environment by combining the structure and rules of the MLS with financial education questions of varying difficulty.

“When you know better you do better.” – Maya Angelou

Heads or Tails?

Yesterday, I spoke about The Fallacy of the Tax Refund. It was important to express my angst with the buffoonery depicted in images of dancing taxpayers because I have never seen that behavior in my firm. Well, since the world is not all black and white – there is another side of the coin if you find yourself with a large tax refund.

Education:

I want to teach you how to use a tax refund to establish a financial foundation and framework for investing and savings. Here is a list of tax-advantaged opportunities to use your tax refund to create your wealth plan.

10 ways to build a nest egg with a tax refund:

Fund a Traditional or Roth IRA account for yourself. (See Lesson #36)

Fund a Roth IRA for your child provided they had any earned income during the tax year. Don’t forget about money earned from babysitting. Consider filing a tax return for your child to take advantage of this opportunity.

Fund a Health Savings Account (HSA) (provided you have a high-deductible health plan. (See Lesson #49)

Purchase of Series I bonds with tax refund money. This can be done automatically through your tax return by attaching Form 8888. (See Lesson #23)

Fund 529 Plan for a child (your child, your niece, your nephew, the kid down the street, etc.) for future education expenses. (See Lesson #43)

Fund a 529 plan for yourself for lifetime learning. (See Lesson #43)

Invest it! (See Lesson #14)

Pay off high-interest credit cards – this will free up additional disposal income sources.

Build up your emergency fund.

Make a charitable contribution.

Whatever you do, please use your presidents wisely!

Resources:

Where’s My Refund? (http://1.usa.gov/1gbazdp) – Get up-to-date refund information using Where’s My Refund? or the IRS2GO mobile app. Where’s My Refund? is updated once every 24 hours, usually overnight. Refunds are generally issued within 21 days after we receive your tax return. You should only call if it has been longer.

Important terms from this lesson:

Term

Definition

Tax Refund

A refund on taxes when the tax liability is less than the taxes paid.

This commercial offends every fiber of my being. The fact that they show a dancing black man, nearly makes me want to throw the remote control right through the television screen. To compound that, they have the audacity to play the early 90s hit from Montell Jordan, This Is How We Do It. Do what?

Who dances when someone pays them money that is owed to them? Am I missing something? Let me get this right. This is as backwards as 3-2-1.

#3 – The GOVERNMENT took more of your money than what was required.

#2 – The GOVERNMENT then forced you to wait nearly a full year to get your money back.

#1 – The GOVERNMENT used your money for free since they did not pay you interest for use of your money – THEY DIDN’T EVEN SAY THANK YOU!

Are you mad now? Good — I want this to offend you the same way that it offends me.

Education:

In today’s lesson, my principle aim is to get you to slam the breaks on Uncle Sam and his cohorts, who exploit you for your hard-earned money. It is time for a prison break; let’s free your money from jail.

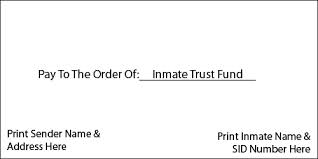

A tax refund is your money being released by the warden; in this case, the government is the warden. Does the warden have the right to take what is rightfully yours and dictate the terms that he will give it back to you? Right now, you are an inmate and the warden has given himself the right to your trust fund.

To make it plain, let’s look at how a tax refund is created.

Tax Refund = Money Withheld/Paid > Money Owed

My clients will attest that I actually prefer if they owe the government money at the end of the day. That way, we are confident that there was no opportunity cost for any money that was paid in or withheld on their behalf. Let me digress for a minute and explain the two main inputs in the above equation.

Money Withheld/Paid

Most employees are required to have their employers WITHHOLD (that means to separate and set aside a portion of your wages) income taxes from your paycheck. This is not to be confused with FICA, which is also a tax, but it has no bearing on your income tax, except in a limited case, which is beyond the scope of this lesson.

Example – Income Tax Withheld

Joan, a single employee earns $1,000 bi-weekly. Based on Joan’s projected annual gross wages, the employer withholds 15% or $150 of her paycheck and gives it to the IRS for Safekeeping until Joan files her annual tax return.

Seems sensible? That crude example appears sensible, but it does NOT take into account any of your other factors such as –

Do you own a home?

Do you support an aging parent?

Do you contribute to a retirement plan?

Do you pay student loan interest?

Do you contribute to a Health Savings Account?

Those questions and more would suggest that your projected gross wages are NOT equal to what your taxable income will ultimately be for the year. That leads into the next topic.

Money Owed

Employees who earn wages are subject to tax on the income that they earn. However, for tax purposes, income has a broader definition. According to IRC Sec. 61, gross income is defined as, “all income from whatever source derived”. You pay income tax on ALL income earned. For most taxpayer, there total income is derived from their employment.

Each April 15th, every taxpayer is called to produce a reconciliation report to the government (federal, state and local), which is the income tax return. Most people know this report as their Form 1040. The sole purpose of the report is to determine who owes whom at the end of the day. It is nothing more than a contest. There are winners and there can be losers. However, in my opinion, the losers are the unsuspecting taxpayers who allowed the government to hold their money without recompense.

Practical Application:

Let us return to the example discussed above. In the example, Joan’s employer has no other information about Joan. The employer does not know that Joan will NOT owe the government when it’s all said and done. However, the employer withheld a total of $3,900 from Joan during the year. Joan now has to file a tax return to get her money back. What could Joan have done with that money during the year if it remained in her hands – this is called “opportunity cost”?

When Joan receives her refund, it will be for the exact amount that was withheld. Translation – her money did not grow. What if she could have invested that money and earned daily-compounded interest? What if she could have put that money in a health savings account? Maybe a bill came up during the year and Joan could have paid it off if she only had her money then.

The point is to change your perception about tax refunds. I never want to see you dancing when you get a refund. I want you to be angry and ask yourself, what could I have done to keep that money in my pocket?

Today’s players:

Government = Warden

People who dance because they get a tax refund = Inmates

Tax Refund = Tax-Free loan to Uncle Sam

Resources:

Important terms from this lesson:

Term

Definition

Tax Refund

A refund on taxes when the tax liability is less than the taxes paid.

Tax Withholding

Income tax withheld from employees’ wages and paid directly to the government by the employer.

Income Tax

Tax levied by a government directly on income, esp. an annual tax on personal income.

Action Step: Read this lesson over and over until you are tired of being an inmate!

On January 19, 2014, I had a tremendous light bulb moment while watching the Suzy Orman show. On January 20, 2014, the light bulb switched to the on position after attending a community discussion on income inequality. That epiphany manifested itself into a blog adeptly named Education and Action – Improving Financial Literacy and Teaching Wealth Building Principles.

As a Certified Public Accountant and Small Business Tax Advisor, I am extremely passionate about matters of financial literacy and economic development. For years, I have remained on the sideline instead of getting into the game and doing my part. Well that has changed and I realize that is up to people like me who have the knowledge to use it to improve literacy in this area and to bridge the wealth gap between the Haves and the Have Nots. For 2014, I vowed to teach one lesson each day for the balance of the year and I have been doing my best to stick with that goal.

The purpose of the Education and Action blog is to provide ERA or Education, Resources and Action steps to help you put the information provided in each daily lesson into practice.

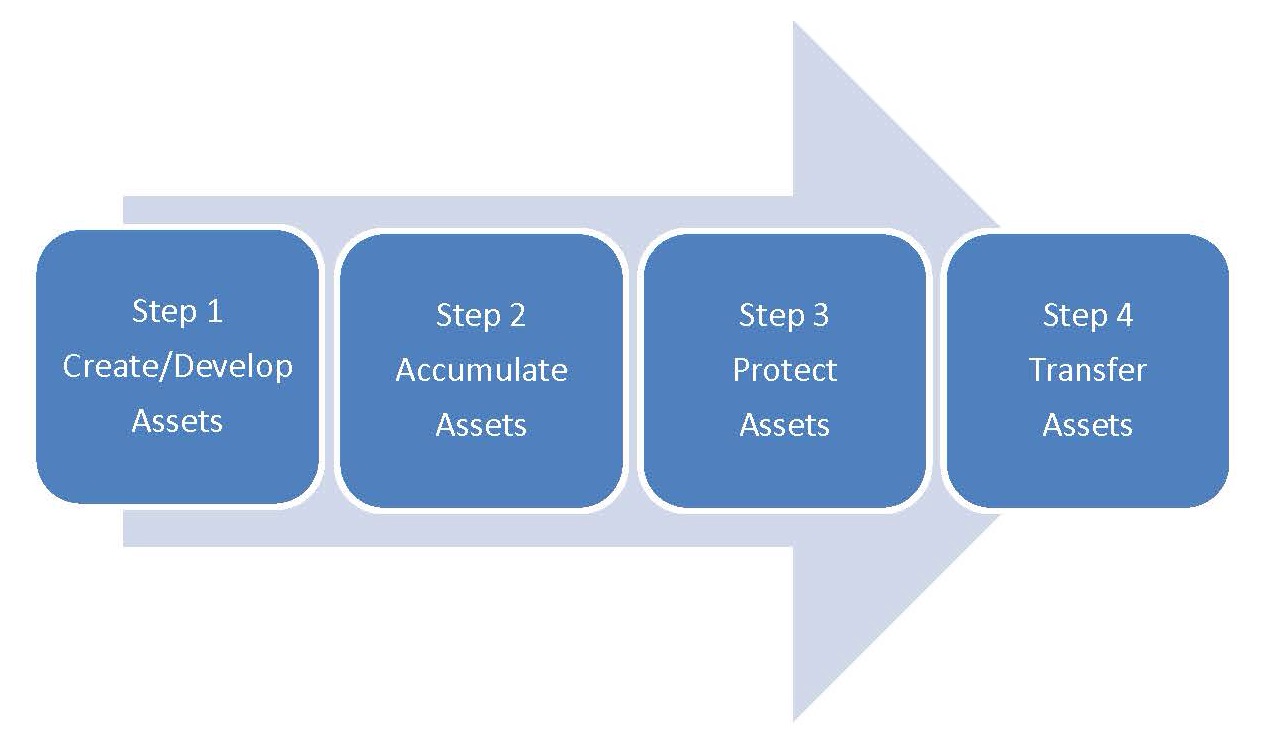

To begin, it was critical to help you see YOUR FUTURE expressed in a journey or your path to financial freedom. The path that I am attempting to illuminate for you is the wealth- building continuum, as expressed in the following flow chart.

Over the past 50 days, I have been teaching on Step 1 – Creating and Developing Assets. It is important that we build a firm foundation to help you pursue your financial goals. On Fridays, I turn my attention to the kids and teaching them valuable financial lessons that they will need to know to live a life of abundance. Saturdays are about encouraging you to keep your eye on the prize and Sundays are to reflect on the week’s lessons.

I hope that you will take some time to join the blog and take advantage of this free information. This is my way to give back all that God has given to me. I appreciate your questions and feedback.

What if you cannot deduct you out-of-pocket medical expenses?

As we continue the march to the April 15th tax deadline, there are several tax benefits that may help you and your family in more ways than one. Let’s face it, the rising costs of healthcare has had a negative impact on our government debt, an employers’ ability to raise wages and rank and file employees’ discretionary income. To mitigate these costs and turn otherwise non-deductible items into tax-deductible items, you should seriously consider the Health Savings Account; one of the most beneficial, yet least understood tax benefits.

Education:

Health Savings Accounts (HSAs) were created in 2003 so that individuals covered by high-deductible health plans (HDHP) could receive tax-preferred treatment of money saved for medical expenses. In today’s lesson, we will discuss how the HSA can be used to help you to save and invest money for future medical expenses. To entice you, it may help to tell you that the HSA is a triple whammy account – it offers three tax advantages.

Tax-free contributions.

Tax-free earnings.

Tax-free expenses (qualified medical expenses).

Now that I have your attention, let’s get into the nuts and bolts of the HSA.

Generally, an adult who is covered by a high-deductible health plan (and has no other first-dollar coverage) may establish an HSA. A high-deductible health plan (HDHP) is a health insurance plan with lower premiums and higher deductibles than a traditional health plan. Those premium and deductible limits are a function of federal regulation. Each year, the IRS releases three key HSA limits – the HSA contribution limit, the HDHP minimum required deductible, and the HDHP out-of-pocket maximum. For 2013, those amounts were as follows:

HSA Contribution Limits. The 2013 annual HSA contribution limit for individuals with self-only HDHP coverage is $3,250 (a $150 increase from 2012), and the limit for individuals with family HDHP coverage is $6,450 (a $200 increase from 2012). HDHP Minimum Required Deductibles. The 2013 minimum annual deductible for self-only HDHP coverage is $1,250 ($50 increase from 2012), and the minimum annual deductible for family HDHP coverage is $2,500 (a $100 increase from 2012).

HDHP Out-of-Pocket Maximum. The 2013 maximum limit on out-of-pocket expenses (including items such as deductibles, co-payments, and co-insurance, but not premiums) for self-only HDHP coverage is $6,250 (a $200 increase from 2012), and the limit for family HDHP coverage is $12,500 (a $400 increase from 2012).

The chart below lists some of the pros and cons of Health Savings Accounts (HSA).

Pros

Cons

Pretax contributions (or tax-deductible contributions, if you’re on your own).

No new contributions allowed to the account after you have signed up for Medicare Part A or Medicare Part B.

Catch-up contributions of $1,000 per individuals age 55 and older.

20% penalty — plus an income-tax bill — if you use any of the money for nonmedical expenses before age 65.

Spend the HSA money tax-free on out-of-pocket medical expenses, such as your deductible, co-payments for medical care and prescription drugs, or bills not covered by insurance, such as vision and dental care.

The account cannot be used to pay insurance premiums (except for limited exception for COBRA premiums).

Most plans provide a debit card and an online bill-payment option.

Few insurers in the Affordable Care Act offer HDHP with HSAs.

No use it or lose it. HSA funds can be carried over from year to year future use.

You must be enrolled in a HDHP to set up an HSA.

No income limits.

Must meet certain Federal guidelines.

Portability (you can keep the money in an HSA account even if you switch jobs.)

20% penalty assessed on excess contributions over the federal limit.

Rollovers allowed from other HSA accounts.

FDIC Insured

Great tool for taxpayers who either do NOT itemize or whose medical expenses fall below the threshold.

Contributions can be made through payroll deductions.

Employer can make contributions to employee accounts.

Resources:

HSAcenter (www.hsacenter.com) – a source of information for consumers looking for HSA options.

Important terms from this lesson:

Term

Definition

High-Deductible Health Plan (HDHP)

A high-deductible health plan (HDHP) is a health insurance plan with lower premiums and higher deductibles than a traditional health plan. Being covered by an HDHP is also a requirement for having a health savings account.

Health Savings Account (HSA)

A health insurance plan that has a high minimum deductible, which does not cover the initial costs or all of the costs of medical expenses.

Action Step: Watch and Learn.

Carve out 18 minutes to watch the video and learn about the awesome benefits providing by using a HSA.

Each Saturday, I will find ways to encourage you to reach your goals. Whether it’s a video, an inspirational message, a poem, or whatever…I want to keep you focused on achieving your goals. Remember that you are the sun and you will provide the light for the people around you to believe. By embarking on this journey, you have already proven that you are a standout in the crowd, a leader. You have shown the desire and willingness to improve your life by implementing new strategies and lessons. I strongly believe that you will be the catalyst for a seismic shift in your family.

Today, our encouragement comes from Steve Jobs and the commencement address that will change your life.

Have a beautiful Saturday!

Action Step: Be encouraged and do not forget to Feed The Pig!

Let’s face it, kids love to spend money! The problem is that there is disconnect in the minds of children between the efforts it takes to earn money and the ease of hand to spend it. That divide can be fixed if we take the time to teach kids about the value of budgeting.

Education:

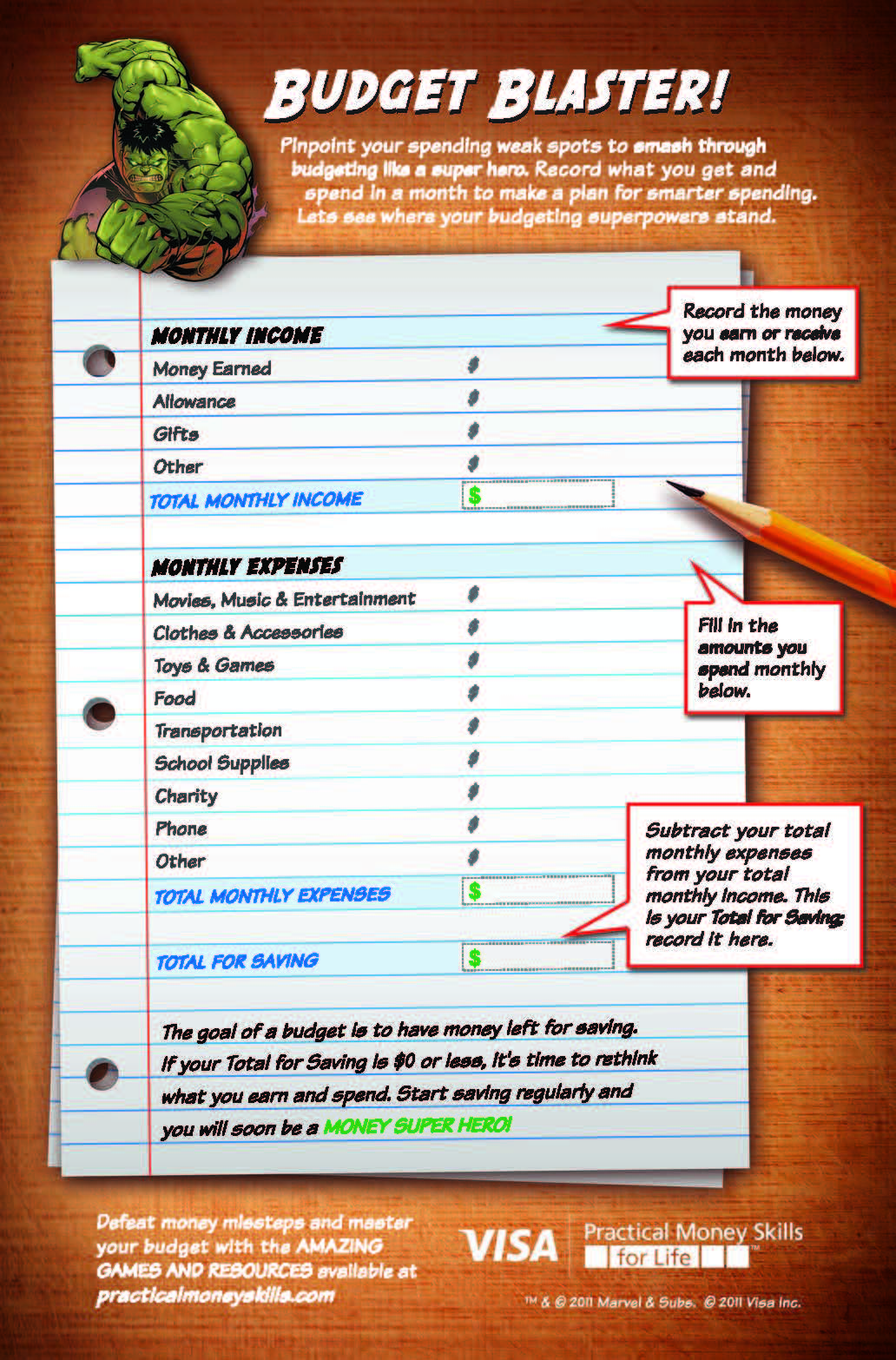

Today’s lesson is to teach kids about the value of Budgeting using Practical Money Skills’ Marvel Budget Blaster. It’s important for kids to understand that unless you are Warren Buffet, money is a finite resource that must be used wisely. This week they want the new Xbox, next week they want the new Air Jordans, and so on. The problem is that parents have failed to paint the yellow brick road for them. The yellow brick road conjures up the journey that Dorothy took in the Wizard of Oz. In reality, parents travel that yellow brick road everyday and it’s called their JOB. Kids don’t often see the work involved with to earn the money, so they don’t see it as a limited resource. In the last few decades, we have moved from a cash society to a credit/debit card society. Though that transition has made it more convenient for parents to consume and do personal banking, kids see the card as an unlimited source of money to make them happy. Today, we will shatter their little perception and teach them how to prioritize the things they want with the money that they have. Kids must learn the difference between two very important terms, disposable income and discretionary income.

Discretionary income – The amount of an individual’s income that is left for spending, investing or saving after taxes and personal necessities (such as food, shelter, and clothing) have been paid. Discretionary income includes money spent on luxury items, vacations and non-essential goods and services.

Disposal income –The amount of personal income an individual has after taxes and government fees, which can be spent on necessities, or non-essentials, or be saved.

Resources:

Marvel Budget Worksheet and Resources – See Action Step below.

Important terms from this lesson:

Term

Definition

Budget

An estimate of income and expenses.

Action Step: Introduce the Marvel Budget Worksheet to your kids

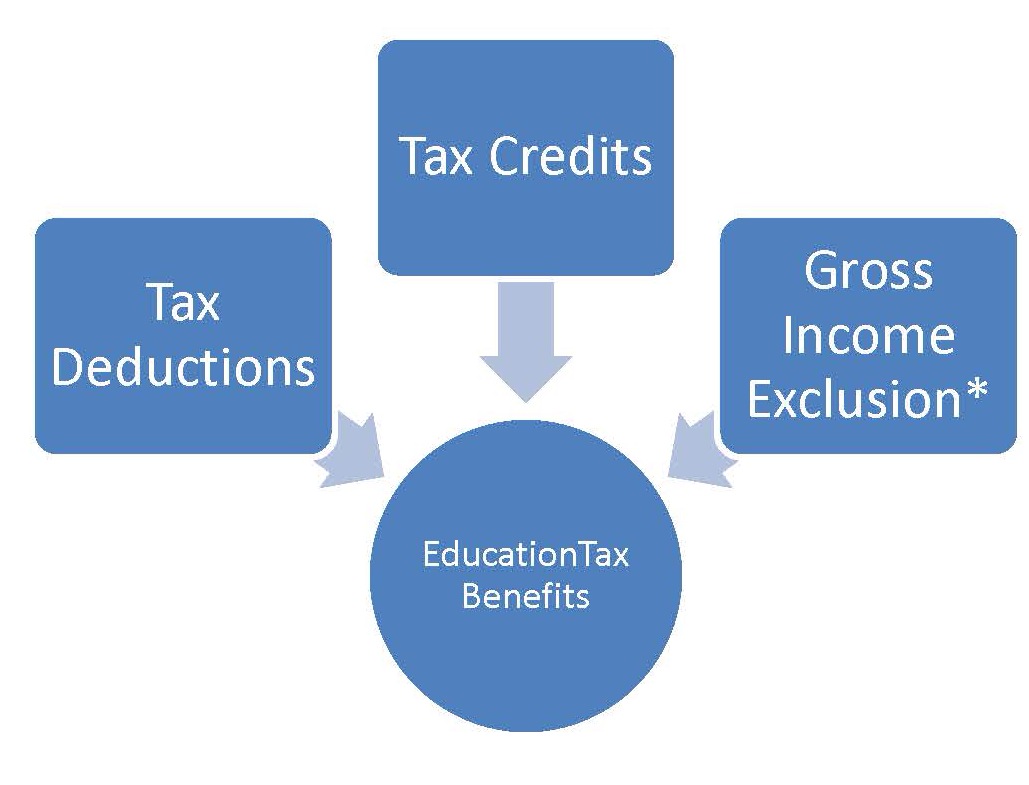

Are you taking advantage of the Education Tax Credits and Deductions?

*To be discussed in a separate lesson.

Tax credits, deductions and savings plans can help taxpayers with their expenses for higher education. The calculus is to choose the one that will yield the best result – the lowest overall tax. That’s it! When coupled with the education savings plans that we discussed earlier this week, parents can use these additional incentives to help curb the cost of a child’s education.

Education:

There are three types of education tax benefits. In today’s lesson, we will help you understand the different benefits that are available to you and how they can be used to save you MONEY!

Tax Benefit

What is does

Preference

Tax Deduction

Reduces the amount of income tax that you pay dollar-for-dollar.

Least preferred

Tax Credit

Reduces the amount of your income that is subject to tax.

Preferred

Gross Income Exclusion

No income tax is paid on this benefit, but you may be prevented from using additional tax-free benefits (deductions and credits).

Most preferred

EDUCATION TAX CREDITS

The diagram below depicts the education-related tax credits that may be available for parents.

It is important that you understand the difference between the education tax credits available to you. To make it easier to compare the two most predominate tax credits currently available, please refer to the comparison chart below.

American Opportunity Tax Credit

Lifetime Learning Credit

Maximum credit

Maximum credit up to $2,500 credit per eligible student.

Up to $2,000 ($4,000 if a student in a Midwestern disaster area) credit per return .

Limit on modified adjusted gross income (MAGI)

$180,000 if married filling jointly adjusted gross $90,000 if single, head of household, or qualifying widow(er).

$120,000 if married filling jointly; $60,000 if single, head of household, or qualifying widow(er).

Refundable or nonrefundable

40% of credit may be refundable; the rest is nonrefundable.

Number of years of postsecondary education

Available only for the first 4 years of postsecondary education.

Available for all years of postsecondary and for courses to acquire or improve job skills.

Number of tax years credit available

Available only for 4 tax years per (including any year(s) Hope Scholarship Credit was claimed.)

Available for an unlimited number of years.

Type of degree required

Student must be pursuing an undergraduate degree or other recognized education credential.

Student does not need to be pursuing a degree or other recognized education credentials.

Number of courses

Student must be enrolled at least half time for at least one academic period beginning during the year.

Available for one or more courses.

Felony drug conviction

No felony drug convictions on student’s records.

Felony drug convictions are permitted.

Qualified expenses

Tuition and required enrollment fees. Course-related books, supplies and equipment do not need to be purchased from the institution to qualify.

Payments for academic periods

Payments made in 2010 for academic periods beginning in 2011 and in the first 3 months of 2011.

Payments made in 2009 for academic periods beginning in 2009 and in the first 3 months of 2010.

Example – Tax Credit

A married couple has a total TAXABLE income is $15,000, which results in a tax bill of $1,500 (10% tax bracket). One spouse took a few courses during the year, for a total tuition and fees of $3,000. The couple is ineligible for the American Opportunity Tax Credit because both spouses have undergraduate degrees. The couple is able to claim the lifetime learning credit.

Total Tax $1, 500

Less: Lifetime Learning Credit <1,500>

Tax After Credits $ 0 <<< Yippie 🙂

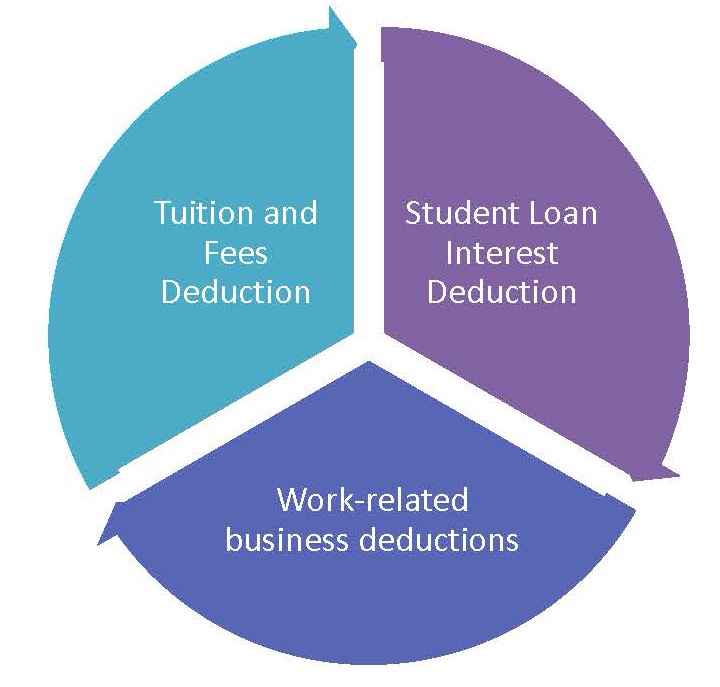

EDUCATION TAX DEDUCTIONS

The diagram below depicts the education-related tax deductions that may be available for parents. The work-related business deductions are beyond the scope of today’s lesson and will be discussed in the near future.

Tuition and Fees Deduction

Pros

Cons

Deduct qualified education expenses paid during the year for yourself, your spouse or your dependent.

You cannot claim this deduction if your filing status is married filing separately or if another person can claim an exemption for you as a dependent on his or her tax return.

Can reduce the amount of your income subject to tax by up to $4,000.

The qualified expenses must be for higher education.

You can claim this deduction even if you do not itemize deductions.

Deduction is phased out if your modified adjusted gross income (MAGI) is more than $80,000 ($160,000 if filing a joint return).

Student-activity fees and expenses for course-related books, supplies and equipment are included in qualified education expenses only if the fees and expenses must be paid to the institution as a condition of enrollment or attendance.

Cannot be claimed if you were a nonresident alien for any part of the year and did not elect to be treated as a resident alien for tax purposes.

Student Loan Interest Deduction

Pros

Cons

Can reduce the amount of your income subject to tax by up to $2,500.

Deduction is phased out if your modified adjusted gross income (MAGI) is less than $75,000 ($150,000 if filing a joint return),

You can claim this deduction even if you do not itemize deductions.

Must be a qualified student loan.

Example – Tax Deduction

A married couple has a total TAXABLE income is $15,000, which results in a tax bill of $1,500 (10% tax bracket). One spouse took a few courses during the year, for a total tuition and fees of $3,000. The couple is ineligible for the American Opportunity Tax Credit because both spouses have undergraduate degrees. The couple is able to claim the lifetime learning credit.

Reduces the amount of income tax you may have to pay dollar-for-dollar.

Tax Deduction

A deduction reduces the amount of your income that is subject to tax, thus generally reducing the amount of tax you may have to pay.

Gross Income Exclusion

No tax is paid on the benefit.

Qualified Student Loan

loan you took out solely to pay qualified education expenses

Action Step: Find out if you are eligible to claim an Education Credit

Use the IRS Interactive Tax Assistant to see if you are eligible to claim an education credit.

This application will help you determine if you are eligible for certain educational credits or deductions including the American Opportunity Credit, the Lifetime Learning Credit and the Tuition and Fees Deduction.

When you have a kid, everyone says “it goes by so fast,” and they’re right. But when you’re talking about college savings, time is on your side when you start early.Prepaid tuition programs are exactly what the name implies: the chance to pay now and buy a certain number of educational credits/years of college at today’s tuition rates. Or so the promotional materials like to say.

Education:

There are several ways to save for the impending costs of college. Some of the investment or savings vehicles that are available to taxpayers are as follows:

1. Coverdell Education Savings Accounts

2. 529 Plans

3. Prepaid College Plans or Prepaid Tuition Plans

In this lesson, we will focus on the Prepaid College Plans, which allow you to prepay for future tuition — typically at today’s prices. A popular college savings vehicles offered at one time in about 20 U.S. states are increasingly running on empty. Currently, only about 19 states still offer a variation of the original plan. Massachusetts, Florida, Mississippi and Washington are the only four states that guarantee their plans through full faith and credit of the state, meaning that if the plan goes bust, the state has to pay the promised tuition amount. The Texas plan is guaranteed by the state universities and colleges. The main issue with this savings vehicle is that the state sponsored plan could go broke before your child receives benefits.

There are pros and cons to prepaid plans. Let’s go through each.

Pros

Cons

Purchase tomorrow’s college education based on today’s costs – lock in future tuition costs

Must attend a college included in the selected plan to receive full benefits

Professionally managed

Often limited to use for only tuition and fees

If your child attends a state college or university, you will have gotten a good deal on tuition.

Not all states have plans.

Low contribution amounts accepted

Declining market returns

Fees

Plan may not guarantee payments when you need them in the future

You could do better investing the money yourself in a college savings plan.

Less control over account.

You run the risk of your state becoming unable to back the funds.

Example (as originally envisioned):

A family could set a tuition rate for colleges within the state’s boundaries at $40,000 for four years when a child is five years old and spend the next 12 years contributing that. If the four-year course costs $60,000 when the child gets to college, the family still only pays $40,000, and will save $20,000.

The prepaid tuition plan is just another option for college savers. Please evaluate all of your options before committing to a strategy to pay for your child’s education.

In the next lesson, we will discuss the tax incentives available to taxpayers to help curb the cost the rising costs of college.