You may know your ABCs, but do you know your ETFs?

The above image depicts a favorite dish from my youth, alphabet soup. Have you ever heard of S&P, NYSE, NASDAQ or FTSE? A better question may be, do you understand what these acronyms mean?

In the world of investing, it can often feel like you are in stuck in a bowl of alphabet soup. When most people see these titles, they are understandably intimidated. In this lesson, I will provide an introduction to Exchange-Traded Funds (ETFs) and discuss how they can be used to help you reach your investment goals.

Education:

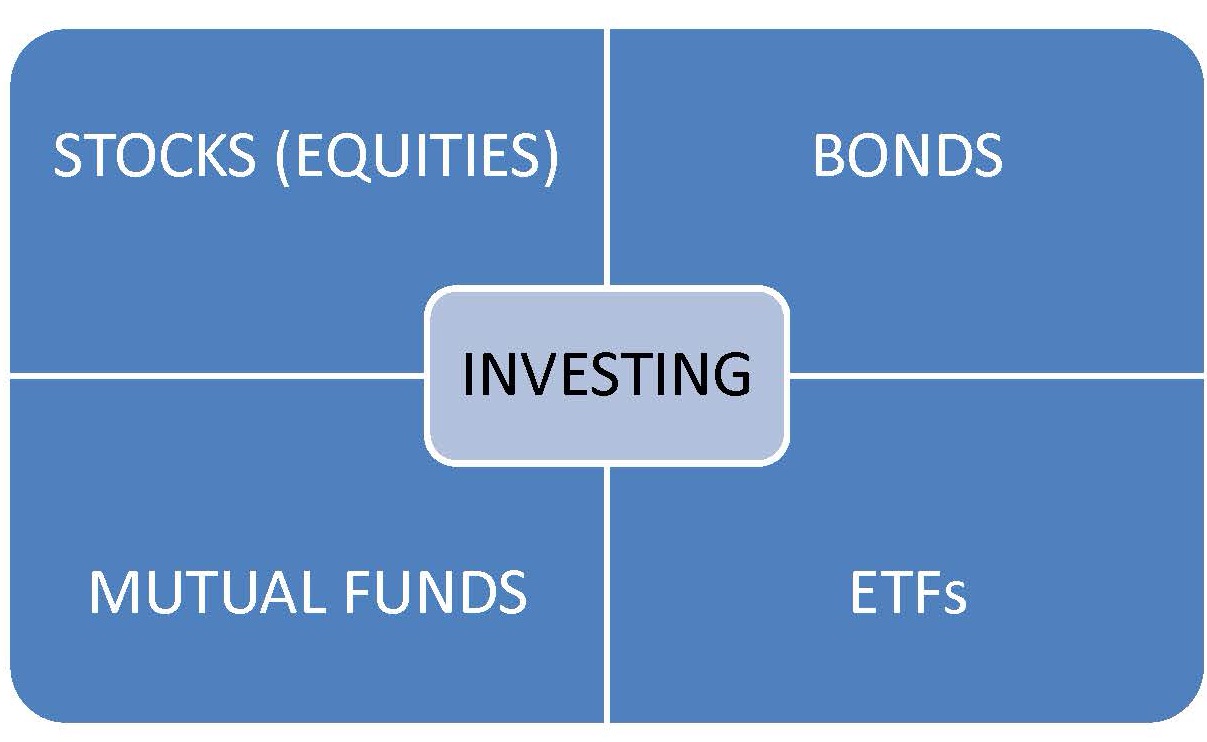

The last category in the investing diagram is ETFs or Exchange Traded Funds.

An exchange-traded fund (ETF) is an investment fund traded on stock exchanges, much like stocks. An ETF holds assets such as stocks, commodities, or bonds. Most ETFs track an index, such as a stock index or bond index. The purpose of an ETF is to match a particular market index. Because, technically, you cannot actually invest in an index, exchange-traded funds allow investors to invest in securities which seek to replicate the index.

In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of the market. Indexes can be based on various categories of stocks. There are the widely known market indexes, such as the Dow Jones Industrial Average, the NASDAQ Composite, or the S&P 500. The Standard & Poor’s 500 (aka S&P 500) is one of the world’s best known indexes, and is the most commonly used benchmark for the stock market. The S&P 500 is a stock market index based on the market capitalizations of 500 large companies having common stock listed on the NYSE or NASDAQ.

When you buy shares of an ETF (e.g. Vanguard S&P 500), you are buying shares of a portfolio that tracks the yield and return of its native index, or the S&P 500 in this instance. Although the Vanguard fund was an example of overall stock market index, there are indexes based on market sectors, such as tech, healthcare, financial; foreign markets; market cap (micro-, small-, mid-, large-, and mega-cap); asset type (small growth, large growth, etc.); even commodities. ETFs provide great flexibility for niche investors.

Benefits of ETFs

- ETFs combine the range of a diversified portfolio with the simplicity of trading a single stock.

- Investors can purchase ETF shares on margin, short sell shares, or hold for the long term.

- Passive management, fund or money manager makes only minor, periodic adjustments to keep the fund in line with its index.

- ETFs mitigate the element of “managerial risk” that can make choosing the right fund difficult.

- ETFs allows you to harness the power of the market itself.

- Fewer administrative costs than actively managed portfolios.

- Tax efficiency – fewer taxable distributions.

- Highly efficient investment

- Diversification

- High liquidity – enabling investors to get into and out of investment positions with minimum risk and expense.

- ETF shares trade exactly like stocks.

- Resources:

CNN Money ETF Finder (http://bit.ly/1oTHzJH) – provides a tool to help investors find funds to fit their individual criteria.

The Vanguard S&P 500 fund – The Fund is a low cost way to gain diversified exposure to the U.S. equity market. The fund invests in 500 of the largest U.S. companies, which span many different industries and account for about three-fourths of the U.S. stock market’s value

Important terms from this lesson:

|

Term |

Definition |

| Exchange Traded Fund (ETF) | A mutual fund that is traded on a stock exchange. |

Action Step: Watch the video, An Introduction to Exchange Traded Funds