Is a HSA right for you?

What if you do NOT itemize your deductions?

What if you cannot deduct you out-of-pocket medical expenses?

As we continue the march to the April 15th tax deadline, there are several tax benefits that may help you and your family in more ways than one. Let’s face it, the rising costs of healthcare has had a negative impact on our government debt, an employers’ ability to raise wages and rank and file employees’ discretionary income. To mitigate these costs and turn otherwise non-deductible items into tax-deductible items, you should seriously consider the Health Savings Account; one of the most beneficial, yet least understood tax benefits.

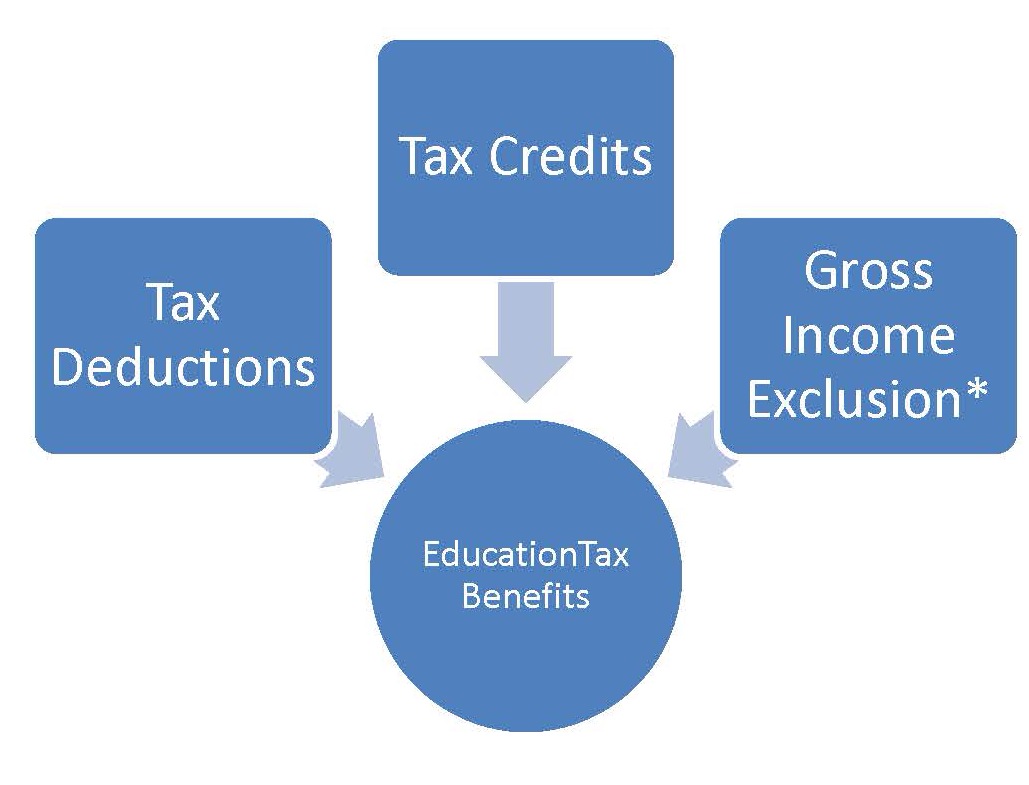

Education:

Health Savings Accounts (HSAs) were created in 2003 so that individuals covered by high-deductible health plans (HDHP) could receive tax-preferred treatment of money saved for medical expenses. In today’s lesson, we will discuss how the HSA can be used to help you to save and invest money for future medical expenses. To entice you, it may help to tell you that the HSA is a triple whammy account – it offers three tax advantages.

- Tax-free contributions.

- Tax-free earnings.

- Tax-free expenses (qualified medical expenses).

Now that I have your attention, let’s get into the nuts and bolts of the HSA.

Generally, an adult who is covered by a high-deductible health plan (and has no other first-dollar coverage) may establish an HSA. A high-deductible health plan (HDHP) is a health insurance plan with lower premiums and higher deductibles than a traditional health plan. Those premium and deductible limits are a function of federal regulation. Each year, the IRS releases three key HSA limits – the HSA contribution limit, the HDHP minimum required deductible, and the HDHP out-of-pocket maximum. For 2013, those amounts were as follows:

HSA Contribution Limits. The 2013 annual HSA contribution limit for individuals with self-only HDHP coverage is $3,250 (a $150 increase from 2012), and the limit for individuals with family HDHP coverage is $6,450 (a $200 increase from 2012).

HDHP Minimum Required Deductibles. The 2013 minimum annual deductible for self-only HDHP coverage is $1,250 ($50 increase from 2012), and the minimum annual deductible for family HDHP coverage is $2,500 (a $100 increase from 2012).

HDHP Out-of-Pocket Maximum. The 2013 maximum limit on out-of-pocket expenses (including items such as deductibles, co-payments, and co-insurance, but not premiums) for self-only HDHP coverage is $6,250 (a $200 increase from 2012), and the limit for family HDHP coverage is $12,500 (a $400 increase from 2012).

The chart below lists some of the pros and cons of Health Savings Accounts (HSA).

|

Pros |

Cons |

| Pretax contributions (or tax-deductible contributions, if you’re on your own). | No new contributions allowed to the account after you have signed up for Medicare Part A or Medicare Part B. |

| Catch-up contributions of $1,000 per individuals age 55 and older. | 20% penalty — plus an income-tax bill — if you use any of the money for nonmedical expenses before age 65.

|

| Spend the HSA money tax-free on out-of-pocket medical expenses, such as your deductible, co-payments for medical care and prescription drugs, or bills not covered by insurance, such as vision and dental care. | The account cannot be used to pay insurance premiums (except for limited exception for COBRA premiums). |

| Most plans provide a debit card and an online bill-payment option. | Few insurers in the Affordable Care Act offer HDHP with HSAs. |

| No use it or lose it. HSA funds can be carried over from year to year future use. | You must be enrolled in a HDHP to set up an HSA. |

| No income limits. | Must meet certain Federal guidelines. |

| Portability (you can keep the money in an HSA account even if you switch jobs.) | 20% penalty assessed on excess contributions over the federal limit. |

| Rollovers allowed from other HSA accounts. | |

| FDIC Insured | |

| Great tool for taxpayers who either do NOT itemize or whose medical expenses fall below the threshold. | |

| Contributions can be made through payroll deductions. | |

| Employer can make contributions to employee accounts. |

Resources:

HSAcenter (www.hsacenter.com) – a source of information for consumers looking for HSA options.

Important terms from this lesson:

|

Term |

Definition |

| High-Deductible Health Plan (HDHP) | A high-deductible health plan (HDHP) is a health insurance plan with lower premiums and higher deductibles than a traditional health plan. Being covered by an HDHP is also a requirement for having a health savings account. |

| Health Savings Account (HSA) | A health insurance plan that has a high minimum deductible, which does not cover the initial costs or all of the costs of medical expenses. |

Action Step: Watch and Learn.

Carve out 18 minutes to watch the video and learn about the awesome benefits providing by using a HSA.