My employer is better than your employer.

I have several friends who work for the government and believe it or not, they still receive the old-fashioned employee pension. It’s no doubt that benefit is a result of a very powerful union. However, for the reminder of us, we are not as lucky and our employers don’t offer the same benefits as others.

In the 20th Century as this country was undergoing a boom in industry and enterprise, the employee pension was a norm. However, over the past several decades, we have seen the disintegration of the good ole’ employee pension plan. In the past, the manufacturing base and the government were the primary providers of employee pension plans or Defined Benefit Plans (DBP). With the advent of globalization, the manufacturing companies in particular, saw their employee costs skyrocket. As a result, many of them relocated their operations to other countries in an effort to reduce employee costs. Unfortunately, the companies who could not relocate, saw their businesses fold and in some cases, bankrupt. Companies who decided to stay and fight had to find a way to lower their employee costs. To accomplish that, one of the most expensive fringe benefits was the employee pension plan. Companies decided to shift the burden of saving for retirement to the employee and with that, Defined Contribution Plans (DCP) were created.

Education:

A QUALIFIED RETIREMENT PLAN is a plan that meets requirements of the Internal Revenue Code and as a result, is eligible to receive certain tax benefits. These plans must be for the exclusive benefit of employees or their beneficiaries. That would make a NON-QUALIFIED RETIREMENT PLAN a plan that does NOT meet requirements of the Internal Revenue Code and as a result, is ineligible to receive certain tax benefits.

There are two kinds of qualified retirement plans: Defined Benefit Plans (DBP) and Defined Contribution Plans (DCP). The easiest way to explain how these plans differ is to ask the question – what is defined?

Defined Benefit Plans (DBP)

Defined Benefit Plans provide for an actuarially determined benefit that you will receive in your retirement years is what is defined. The classic example of a defined benefit plan is the old employee pension (refer to the introduction). With an employee pension plan, the employer agrees to pay the employee a defined amount during their retirement in exchange for a certain number of years of service. The years of service are also known as, the vesting period, which is beyond the scope of today’s lesson. Moreover, a defined benefit plan means that the Plan specifies, or defines, a formula for calculating the benefit that will be paid to you.

The Plan’s formula for determining the amount of your pension benefit includes:

- Your years of pension service.

- Your pensionable pay.

- Your estimated Social Security benefit.

DBP Formula:

Your basic pension benefit is determined by this formula:

- 1.6% x years of pension service x final average pensionable pay

- minus

your Social Security offset - Your basic pension benefit is a monthly amount payable to you starting at age 65 as a Basic Annuity. If you elect to begin your benefit before age 65 or elect a different payment option, the basic pension benefit may be adjusted.

Example — Basic Pension Benefit:

Here is an example of how the basic pension benefit is calculated.

Pat has 30 years of pension service, final average pensionable pay of $7,000 a month and a Social Security offset of $662 a month.

1.6% x 30 years x $7,000 $ 3,360

Less: Social Security offset – 662

Pat’s monthly basic pension $ 2,698

| Advantages |

Disadvantages |

| Employer MUST contribute | Must be vested to receive future benefits |

| Employee does not contribute | Employee has no control |

| Allows loans | Distributions taxable in retirement years |

| Virtually free employee benefit | No rollovers |

| No control of benefit after termination of job |

Defined Contribution Plans (DCP)

Defined Contribution Plans provide for a fixed or discretionary contribution to an account balance maintained on behalf of each employee. Plans with a 401(k) employee savings feature allow employees to contribute a portion of their compensation to the plan. Some employers match employee 401(k) contributions. The ultimate retirement benefit is based upon the periodic distributions, which can be provided by the accumulated account balance upon retirement.

DCP Formula:

Starting with the basics, all retirement plans are based on a very simple formula:

C + I = B

C stands for contributions made. I represents investment earnings—in other words, the market returns generated by investing the contributions. And B is the benefits paid out to the retiree.

Example – Basic Contribution:

If you earn $35,000 a year and your employer limits contributions to 20 percent of pay, you could only contribute up to $7,000 a year ($35,000 X 0.20 = $7,000). If you employer matches your contributions up to 3 percent of pay, then you would have a total of $8,050 contributed a year.

|

Advantages |

Disadvantes |

| Employer may contribute (match) | No vesting required on employee contributions |

| Employee has control | Distribution are taxable |

| May allows loans and hardship withdrawals | Early distribution penalties may apply |

| Pretax contributions | Investment options may be limited |

| Tax-Deferred Earnings | Required Minimum Distributions |

| Rollovers allowed (with exceptions) |

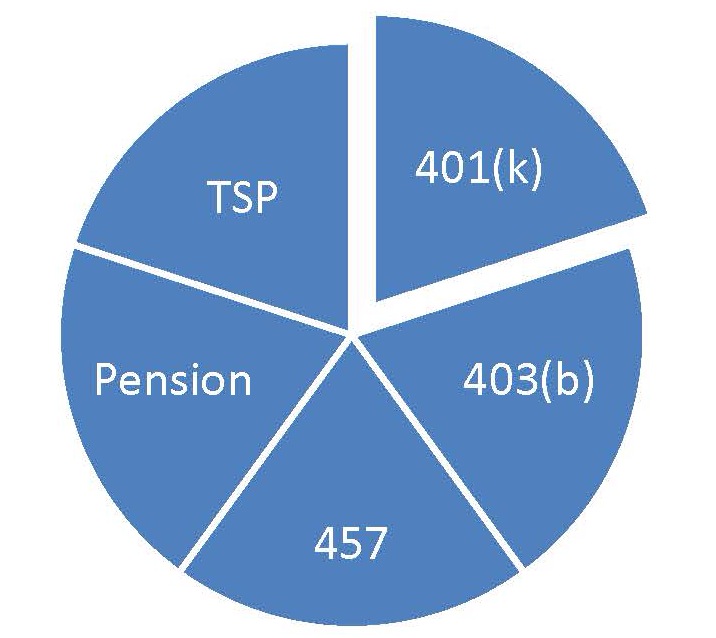

Some examples of defined-contribution plans are 401(k) plans (most common type of DCP), 403(b), 457s, and TSPs.

In the next lesson, we will discuss President’s Obama new retirement initiative, the MyRA account.

Resources:

The Pension Benefit Guarantee Corporation (PBGC). Defined benefit plans are the only type of pension insured by the PBGC. The insurance works similarly to the federal deposit insurance that backs up your bank accounts. If your plan is covered and the sponsoring company goes bust, PBGC will take over benefit payments up to a maximum amount. The insurance protection helps make your pension more secure, but it is not a full guarantee that you will get what you expected.

Important terms from this lesson:

|

Term |

Definition |

| Defined Benefit Plan (DBP) | An employer-sponsored retirement plan where employee benefits are sorted out based on a formula using factors such as salary history and duration of employment. |

| Defined Contribution Plan (DCP) | A retirement plan in which a certain amount or percentage of money is set aside each year by a company for the benefit of the employee. |

| Qualified Retirement Plan | Eligible to receive certain tax benefits. |

| Non Qualified Retirement Plan | Ineligible to receive certain tax benefits. |

| 401(k) | 401(k)s are the version that corporations offer to their employees. |

| 403(b) | 403(b)s are for employees of public education entities and most other nonprofit organizations. |

| 457 | 457s are for state and municipal employees, as well as employees of qualified nonprofits. |

| Thrift Savings Plans (TSPs) | Thrift Savings Plans (TSPs) are for federal employees. |

Action Step: Watch and Learn.