Happy Valentine’s Day!

Given that today is Valentine’s Day, I will be the first to admit that bonds are not the sexiest investment to talk about. However, it is critical that you understand how this fixed income security fits into your overall investment portfolio. First, it provides stability to counterbalance other more risky investments in your portfolio. Even the riskiest people among us, loves a little certainty. This past week was spent demystifying the world of bonds to make it more accessible to you. You may not like bonds now, but if you live long enough, then they will make a great bed fellow in your latter years.

Education:

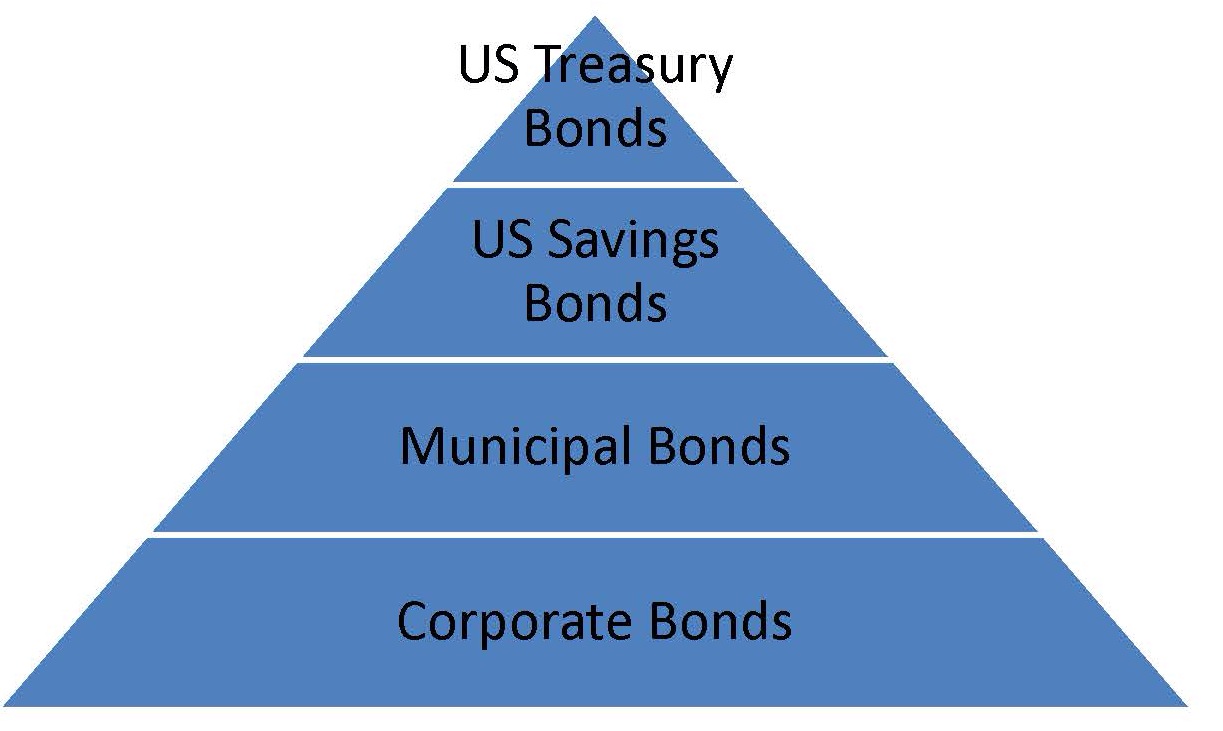

In this lesson, we will close out out the bond pyramid that was introduced in Lesson #22. In case you forgot the hierarchy, let’s take another look.

I dedicated the last two lessons to discussing the benefits of investing with our very own United States Government. It felt good for the government to owe us some money for a chance. As a creditor of the U.S. Government holding either Treasury Securities or Savings Bonds, your money is in good hands. We can now shift our focus to the distant relative of those secure investments – Municipal Bonds and Corporate Bonds.

Municipal Bonds, or Munis are debt securities issued by a state, municipality or county to finance its capital expenditures. Municipal bonds are exempt from federal taxes and from most state and local taxes, especially if you live in the state in which the bond is issued. Municipal bonds may be used to fund expenditures such as the construction of highways, bridges or schools. “Munis” are bought for their favorable tax implications, and are popular with people in high income tax brackets.

The primary reason that people invest in Municipal Bonds is – Tax-exempt interest.

EXAMPLE: If you buy $10,000 worth of municipal bonds with a 4% coupon, the $400 you receive every year is tax-free. Kaboom! Anytime you can earn tax-free income, that’s a Kaboom!

Corporate Bonds are debt securities issued by a corporation and sold to investors. The backing for the bond is usually the payment ability of the company, which is typically money to be earned from future operations. In some cases, the company’s physical assets may be used as collateral for bonds. Corporate bonds are considered higher risk than government bonds. As a result, interest rates are almost always higher, even for top-flight credit quality companies.

The primary reason that people invest in Corporate Bonds is – Higher Interest Rates.

EXAMPLE: If you buy $10,000 worth of municipal bonds with a 4% coupon, you will receive $400 in interest. However, if you buy $10,000 worth of corporate bonds with a 6% coupon, you will receive $600 in interest.

It’s not rocket science. You are simply looking for the angel which will earn you more money. That’s it!

While those definitions provide a conceptual framework, bonds are quite complicated and these lessons serve only to introduce these investment alternatives to you. You certainly do not want to attempt to invest in Municipal or Corporate Bonds without a sound financial advisor (refer to Lesson #18).

Resources:

MunicipalBonds.com (http://www.municipalbonds.com/) – The Premiere Site for Municipal Bond Investors

Important terms from this lesson:

|

Term |

Definition |

| Municipal Bond | A debt security issued by a state, municipality or county to finance its capital expenditures |

| Corporate Bond | A debt security issued by a corporation and sold to investors. |

Action Step: Read the article entitled, ‘The 5 Basic Elements of Bond Investing’