“Train up a child in the way he should go, And when he is old he will not depart from it. “ – Proverbs 22:6

It is no coincidence that I grew up to become a Certified Public Accountant because my fascination with money began at a very young age. When I was a kid, one of the things that my family would do is play board games. One of my favorite board games was Monopoly, the quintessential game about MONEY. I’m sure that Charles Darrow, the creator of Monopoly, never envisioned how vital his board game would be to teaching the value of a dollar to the youth of America and ultimately the world. I can proudly say that I still own this board game and it continues to excite me to play it with friends.

Education:

Today’s lesson will focus on Monopoly. Through the use of Monopoly money, the game teaches the value of a dollar and its PURCHASING POWER. In addition, the game teaches about life through various aspects of society and wealth, including:

The Bank (teaches the central purpose of the banking system, to lend and exchange money)

The Banker (the individuals who make money decisions that affect your life)

Chance (many things in life as a result of chance)

Community Chest (the importance of the community to your success)

Jail (the consequences of making bad moves and decisions in life)

Properties (how ownership creates wealth)

Mortgaging (the cost of property ownership – evaluating mortgage options)

Bankruptcy (the consequences of poor financial management)

Utilities (municipal obligations)

Infrastructure (real estate and railroads)

Later versions of the game teach about banking, the stock market, currencies, international markets, etc. As our financial world changes, the game evolves to teach the new batch of kids about the world. Never underestimate the value of games to teach critical lessons about life.

Let’s do more to help Americans save for retirement. Today, most workers don’t have a pension. A Social Security check often isn’t enough on its own. And while the stock market has doubled over the last five years, that doesn’t help folks who don’t have 401(k)s. That’s why … I will direct the Treasury to create a new way for working Americans to start their own retirement savings: myRA.

— President Barack Obama, State of the Union, January 28, 2014

It is a fact that most Americans, namely low-income citizens, have not and do not adequately save for retirement. I fear that we are becoming an entitlement nation where we shift personal responsibility to someone other than the man or woman in the mirror. As we discussed in Lesson #36, Social Security is a fleeting reality for many of us. In thirty or forty years, it may be a figment of a distant past. It’s YOUR responsibility to prepare yourself and your family for retirement. It is NOT the government’s responsibility to provide for you in your retirement years. Given that many of you will live up to twenty and some thirty years after your retire, it is imperative that you begin to take advantage of any opportunity provided to save for your golden years.

President Obama would like to help American save for retirement. Listen to him describe the initiative in his own words.

Low rate of return (rate tied to US Treasury Securities)

Contribution directly from your paycheck

Opportunity costs

Safe, no risk

Accounts will solely invest in government savings bonds

Government guarantee against loss of principal

Contributions limited to $5,500 per year

Great for low-income taxpayers

It will not be enough for retirement – additional retirement assets will be needed

May qualify some taxpayers for Retirement Savings Tax Credit

Potential automatic enrollment for workers

Function likea Roth IRA (invest after-tax dollars and withdraw the money in retirement tax-free)

Portability (workers will be able to keep the accounts when they switch jobs or contribute to the same account from multiple part-time jobs)

Tax-Free distribution of original contributions

No Fees

Practical Example:

With an average 2% interest rate, for example, a worker contributing $100 a month would accumulate around $6,300 in savings after five years, including around $300 in interest.

Resources:

Whitehouse.gov – For the latest information about the MyRA Savings Plan.

Important terms from this lesson:

Term

Definition

MyRA Savings Plan

MyRA is a new type of savings account for Americans who don’t have access to an employer-sponsored retirement savings plan.

I have several friends who work for the government and believe it or not, they still receive the old-fashioned employee pension. It’s no doubt that benefit is a result of a very powerful union. However, for the reminder of us, we are not as lucky and our employers don’t offer the same benefits as others.

In the 20th Century as this country was undergoing a boom in industry and enterprise, the employee pension was a norm. However, over the past several decades, we have seen the disintegration of the good ole’ employee pension plan. In the past, the manufacturing base and the government were the primary providers of employee pension plans or Defined Benefit Plans (DBP). With the advent of globalization, the manufacturing companies in particular, saw their employee costs skyrocket. As a result, many of them relocated their operations to other countries in an effort to reduce employee costs. Unfortunately, the companies who could not relocate, saw their businesses fold and in some cases, bankrupt. Companies who decided to stay and fight had to find a way to lower their employee costs. To accomplish that, one of the most expensive fringe benefits was the employee pension plan. Companies decided to shift the burden of saving for retirement to the employee and with that, Defined Contribution Plans (DCP) were created.

Education:

A QUALIFIED RETIREMENT PLAN is a plan that meets requirements of the Internal Revenue Code and as a result, is eligible to receive certain tax benefits. These plans must be for the exclusive benefit of employees or their beneficiaries. That would make a NON-QUALIFIED RETIREMENT PLAN a plan that does NOT meet requirements of the Internal Revenue Code and as a result, is ineligible to receive certain tax benefits.

There are two kinds of qualified retirement plans: Defined Benefit Plans (DBP) and Defined Contribution Plans (DCP). The easiest way to explain how these plans differ is to ask the question – what is defined?

Defined Benefit Plans (DBP)

Defined Benefit Plans provide for an actuarially determined benefit that you will receive in your retirement years is what is defined. The classic example of a defined benefit plan is the old employee pension (refer to the introduction). With an employee pension plan, the employer agrees to pay the employee a defined amount during their retirement in exchange for a certain number of years of service. The years of service are also known as, the vesting period, which is beyond the scope of today’s lesson. Moreover, a defined benefit plan means that the Plan specifies, or defines, a formula for calculating the benefit that will be paid to you.

The Plan’s formula for determining the amount of your pension benefit includes:

Your years of pension service.

Your pensionable pay.

Your estimated Social Security benefit.

DBP Formula:

Your basic pension benefit is determined by this formula:

1.6% x years of pension service x final average pensionable pay

minus

your Social Security offset

Your basic pension benefit is a monthly amount payable to you starting at age 65 as a Basic Annuity. If you elect to begin your benefit before age 65 or elect a different payment option, the basic pension benefit may be adjusted.

Example — Basic Pension Benefit:

Here is an example of how the basic pension benefit is calculated.

Pat has 30 years of pension service, final average pensionable pay of $7,000 a month and a Social Security offset of $662 a month.

1.6% x 30 years x $7,000 $ 3,360

Less: Social Security offset – 662

Pat’s monthly basic pension $ 2,698

Advantages

Disadvantages

Employer MUST contribute

Must be vested to receive future benefits

Employee does not contribute

Employee has no control

Allows loans

Distributions taxable in retirement years

Virtually free employee benefit

No rollovers

No control of benefit after termination of job

Defined Contribution Plans (DCP)

Defined Contribution Plans provide for a fixed or discretionary contribution to an account balance maintained on behalf of each employee. Plans with a 401(k) employee savings feature allow employees to contribute a portion of their compensation to the plan. Some employers match employee 401(k) contributions. The ultimate retirement benefit is based upon the periodic distributions, which can be provided by the accumulated account balance upon retirement.

DCP Formula:

Starting with the basics, all retirement plans are based on a very simple formula:

C + I = B

C stands for contributions made. I represents investment earnings—in other words, the market returns generated by investing the contributions. And B is the benefits paid out to the retiree.

Example – Basic Contribution:

If you earn $35,000 a year and your employer limits contributions to 20 percent of pay, you could only contribute up to $7,000 a year ($35,000 X 0.20 = $7,000). If you employer matches your contributions up to 3 percent of pay, then you would have a total of $8,050 contributed a year.

Advantages

Disadvantes

Employer may contribute (match)

No vesting required on employee contributions

Employee has control

Distribution are taxable

May allows loans and hardship withdrawals

Early distribution penalties may apply

Pretax contributions

Investment options may be limited

Tax-Deferred Earnings

Required Minimum Distributions

Rollovers allowed (with exceptions)

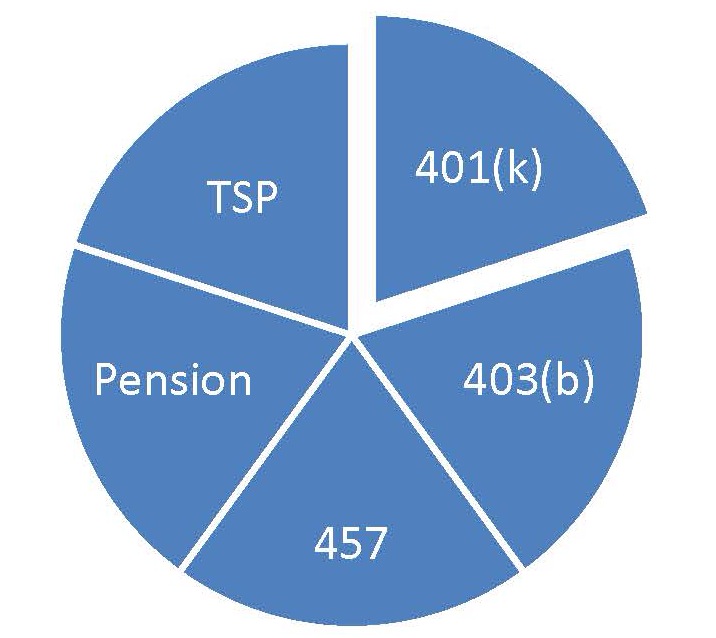

Some examples of defined-contribution plans are 401(k) plans (most common type of DCP), 403(b), 457s, and TSPs.

In the next lesson, we will discuss President’s Obama new retirement initiative, the MyRA account.

Resources:

The Pension Benefit Guarantee Corporation (PBGC). Defined benefit plans are the only type of pension insured by the PBGC. The insurance works similarly to the federal deposit insurance that backs up your bank accounts. If your plan is covered and the sponsoring company goes bust, PBGC will take over benefit payments up to a maximum amount. The insurance protection helps make your pension more secure, but it is not a full guarantee that you will get what you expected.

Important terms from this lesson:

Term

Definition

Defined Benefit Plan (DBP)

An employer-sponsored retirement plan where employee benefits are sorted out based on a formula using factors such as salary history and duration of employment.

Defined Contribution Plan (DCP)

A retirement plan in which a certain amount or percentage of money is set aside each year by a company for the benefit of the employee.

Qualified Retirement Plan

Eligible to receive certain tax benefits.

Non Qualified Retirement Plan

Ineligible to receive certain tax benefits.

401(k)

401(k)s are the version that corporations offer to their employees.

403(b)

403(b)s are for employees of public education entities and most other nonprofit organizations.

457

457s are for state and municipal employees, as well as employees of qualified nonprofits.

Thrift Savings Plans (TSPs)

Thrift Savings Plans (TSPs) are for federal employees.

I am the captain of my soul.” – Invictus, William Ernest Henley

The 1935 Social Security Act signed into law by President Franklin D. Roosevelt was a game changer in this nation. Having witnessed the devastation caused by the great depression, the Act was an attempt to limit what were seen as dangers in the modern American life, including old age, poverty, unemployment, and the burdens of widows and fatherless children. By signing this Act on August 14, 1935, President Roosevelt became the first president to advocate federal assistance for the elderly.

Fast forward to the 21st Century; our relationship to Social Security has changed drastically. Most Americans realize that Social Security as our grandparents knew it, may not be around or may be materially different by the time we are eligible to receive it. As a result, as a prudent wealth builder, you should proceed as if Social Security will NOT be available.

So how would you save for retirement as if there were NO social security available to you?

Take your retirement into your own hands!

Education:

I love America! I love this country because you can be anything that you want to be, including wealthy. There are no barriers to creating wealth for yourself to enjoy now or in your retirement years. The only problem is that many people don’t take advantage of the information available to them to better their situation. Today’s lesson is about taking your retirement into your own hands. One of the products that will enable you to be the master of your fate and the captain of your soul is the INDIVIDUAL RETIREMENT ACCOUNT (IRA). The two type of IRAs are the Traditional IRA and the Roth IRA.

Traditional and Roth IRAs

Traditional and Roth IRAs allow you to save money for retirement. This chart highlights some of their similarities and differences.

Features

Traditional IRA

Roth IRA

Who can contribute?

You can contribute if you (or your spouse if filing jointly) have taxable compensation but not after you are age 70½ or older.

You can contribute at any age if you (or your spouse if filing jointly) have taxable compensation and your modified adjusted gross income is below certain amounts.

Are my contributions deductible?

You can deduct your contributions if you qualify.

Your contributions aren’t deductible.

How much can I contribute?

The most you can contribute to all of your traditional and Roth IRAs is the smaller of:

for 2012, $5,000, or $6,000 if you’re age 50 or older by the end of the year ($5,500 or $6,500 for 2013); or

your taxable compensation for the year.

What is the deadline to make contributions?

Your tax return filing deadline (not including extensions). For example, you have until April 15, 2013, to make your 2012 contribution.

When can I withdraw money?

You can withdraw money anytime.

Do I have to take required minimum distributions?

You must start taking distributions by April 1 following the year in which you turn age 70½ and by December 31 of later years.

Not required if you are the original owner.

Are my withdrawals and distributions taxable?

Any deductible contributions and earnings you withdraw or that are distributed from your traditional IRA are taxable. Also, if you are under age 59 ½ you may have to pay an additional 10% tax for early withdrawals unless you qualify for an exception.

None if it’s a qualified distribution (or a withdrawal that is a qualified distribution). Otherwise, part of the distribution or withdrawal may be taxable. If you are under age 59 ½, you may also have to pay an additional 10% tax for early withdrawals unless you qualify for an exception.

Tax Planning Tip – (When to contribute to a Traditional IRA or a Roth IRA.)

Traditional IRA (Pretax contributions)

High tax bracket years

Money is not needed within a five-year window

Roth IRA (After-tax contributions)

Make contribution if you are in a low tax bracket

Advantages of IRA Accounts:

Ability to invest in a variety of assets – other plans like 401(k)s are limited to mutual fund types of investment. The IRA will enable you to invest in almost any type of asset including gold, other businesses, etc.

Allows rollovers from other qualified retirement plans (term will be discussed in the next lesson).

Earnings grow tax free (Roth IRA only)

Distribution allowed to pay for qualified education expenses or medical expenses.

Easy setup – virtually no administration involved.

Offered by nearly all financial institutions.

Disadvantages of IRA Accounts:

No loans are permitted.

Cannot rollover to a 401(k) type plan.

Traditional IRA and Roth IRA (other than rollover IRAs) may be subject to creditor claims, including IRS levies.

Subject to early distribution penalties, unless exception applies.

Required Minimum Distributions (Traditional IRA only)

Fees

Resources:

RothIRA.com – Online resource to help investors understand Individual Retirement Accounts.

Important terms from this lesson:

Term

Definition

Individual Retirement Account (IRA)

An investing tool used by individuals to earn and earmark funds for retirement savings.

Traditional IRA

An individual retirement account (IRA) that allows individuals to direct pretax income, up to specific annual limits, toward investments that can grow tax-deferred (no capital gains or dividend income is taxed). Individual taxpayers are allowed to contribute 100% of compensation up to a specified maximum dollar amount to their Traditional IRA. Contributions to the Traditional IRA may be tax-deductible depending on the taxpayer’s income, tax-filing status and other factors.

Roth IRA

An individual retirement plan that bears many similarities to the traditional IRA, but contributions are not tax deductible and qualified distributions are tax free. Similar to other retirement plan accounts, non-qualified distributions from a Roth IRA may be subject to a penalty upon withdrawal.

Hope is a great thing, but hope alone won’t get you to your goal. Saving for retirement is all about hope coupled with some concrete action. I can hear you grumbling about today’s excursion into the world of retirement. If I close my eyes, I can visual you you saying, “I have thirty years until I retire so why should I save now”. While I empathize, it’s never too early to begin saving for retirement. Did you know that in 2011, the average life expectancy in the United States was 78.64 years (World Bank)? Let’s do a bit of math.

Normal Retirement Age 65

Average Life Expectancy 78.64

Difference 13.64 years

Sure, that’s pretty modest given the fact that people are living longer and longer these days, many well into their eighties and nineties. If someone had a crystal ball and they told you that you would live to see your 90th birthday, would you have enough money to last for 25 years? I’m sure that there are some people out there who could answer in the affirmative, but for the majority of us, this is nothing more than wishful thinking at this point.

Education:

In Lesson #1, I introduced the wealth-building continuum. Right now, you are most likely in the ACCUMULATION phase of your life. Retirement, on the other hand, can be viewed as the DISTRIBUTION phase of your life. Simply stated, your accumulation years are your working years. This is the time when you can make mistakes and then make the adjustments needed to ensure that you have or are creating the resources that you will need to be comfortable during your retirement years.

The reason that we want to begin saving for retirement now is that we want to take advantage of something called the, Time Value of Money (TVM). The TVM is the idea that money available today is worth more than the same amount in the future due to its potential earning capacity. The earning capacity is why you want to get into the game now. If you determine that you need $1 million dollars during your retirement years and you only have $1,000 saved now, that would suggest that you have some serious work to do. However, it’s not impossible, if you begin saving for retirement today.

Since you have twenty to thirty years to earn and preserve money, you can take on more risk in an effort to increase your earning capacity during the accumulation phase. Once you reach the protection phase of your life, your focus will shift to preserving what was earned during the accumulation phase. This long-term horizon gives you maximum flexibility to take advantage of the products that are available to help you reach your goal.

For an example of the Time Value of Money, click the link below to see a brief video and example.

This week, we will concentrate on creating, understanding and exploring retirement assets. Some of the things that we will discuss this week will include the following:

Defined Benefit Plan vs. Defined Contribution Plan

IRA vs. Roth IRA

Qualified Retirement Plan vs. Non-qualified Retirement Plan

401(K), including UniK or Solo 401(k) Plans

403(B)

457 Plans

SEP

SIMPLE

Keogh

MyRA (President Obama’s new retirement option)

Tax Benefits of saving for retirement

Your number – how much you will need to retire.

Resources:

KMSYKESCPA.COM Knowledge Center – Financial calculators and guides available to help educate

Important terms from this lesson:

Term

Definition

Time Value of Money (TVM)

The idea that money available today is worth more than the same amount in the future due to its potential earning capacity.

Action Step: Calculate your life expectancy.

Click of the link and fill in the questions to calculate your life expectancy.

Each Saturday, I will find ways to encourage you to reach your goals. Whether it’s a video, an inspirational message, a poem, or whatever…I want to keep you focused on achieving your goals. Remember that you are the sun and you will provide the light for the people around you to believe. By embarking on this journey, you have already proven that you are a standout in the crowd, a leader. You have shown the desire and willingness to improve your life by implementing new strategies and lessons. I strongly believe that you will be the catalyst for a seismic shift in your family.

Today, our encouragement comes from Vanguard chairman and CEO Bill McNabb and the Five-Minute Rule of Investing

“I believe the children are our future. Teach them well and let them lead the way.” – Whitney Houston

If you remember, the idea of this blog was originally conceived when a child called into the Suzy Orman show. If you don’t recall, then go back to my very first post and read where the inspiration originated.

I have been providing lessons to you each day in an effort to raise your level of financial literacy. Yesterday, it dawned on me that these lessons are not isolated for adults, but are more effective when taught to children because as the song lyrics go, “they are the future, teach then well and let them lead the way.” With that said, each Friday’s lesson from today forth will be to teach financial principles for kids. However, I’m depending on you, parents, to share this information with them. Make financial literacy a priority in your household.

Let’s begin from the beginning – teach your child how to save!

Education:

Let’s face it, kids like to spend money! I don’t think there is a parent who would disagree with that sentiment. The problem is that kids are taught to spend because they are constantly inundated with commercials and advertising campaigns designed to excite the dollars right out of their parent’s pockets and pocketbooks. I don’t blame the kids, heck…they are just being kids…I blame YOU! Yes, you the parents, because many of you have never taught them to SAVE –solvency through appreciating assets of value in my estate.

S – Solvency

A – Assets

V – Value

E – Estate

Teach you child that COINS are there friends! If they learn to associate a simple coin with money in the bank, that association will help them to develop a lifestyle of saving!

What are you teaching your child or children about money? Are you teaching them negative or positive aspects of money? How are your reinforcing their understanding of money? These are questions that you need to ask yourself. If you don’t like the answer, then I challenge you to take advantage of Financial Literacy Friday for Kids!

Resources:

Kids’ Money (http://kidsmoney.org/) – Kids’ Money is an interactive resource for parents, teachers, teens, kids, organizations and international visitors designed to help children develop successful money management habits and become financially responsible adults.

Important terms from this lesson:

Term

Definition

Solvency

In kids’ terms – Having more money and assets than debts!

Estate

In kids’ terms – Everything that you own of value.

Action Step: Make SAVING fun and for a purpose! Here are your instructions.

Buy your child or children a PIGGY BANK. Yes, a piggy bank!

Buy your child a calendar.

Discuss what it means to SAVE with your child – Solvency through appreciating Assets of Value of my Estate.

For 2014, circle one day in the calendar every month so that you have 11 days circled (sinced we are already in the month of February) – this is your official TAKE A KID TO THE BANK DAY.

Find a bank like TD Bank with a penny arcade.

Every month on TAKE A KID TO THE BANK DAY, have your child go to the penny arcade and deposit every coin that they found, earned, or raised during the month. When you get your deposit receipt, use it to open up a SAVINGS (what else) account for your kid.

Repeat this step every month. Once received, go over the receipts with your child so that they can understand how money is saved.

If you have a teenager, then no worries. Just skip the piggy bank portion, but follow everything else. They need to know that one day of the month is set aside to SAVE!

“To improve is to change. To perfect is to change often.” – House of Cards

In the last lesson, we began our introduction to Exchange Traded Funds. While Lesson #30 got the proverbial ETF ball rolling, there was just too much information to fit into one lesson. So, today we will continue exploring the world of ETFs. ETFs are gamechangers! If you want to be an effective investor, then you have to change your approach to investing. The old way of thinking would suggest that if you like Apple, then buy a lot of Apple stock. Well, that’s great if you can afford it. However, we learned in Lesson #16, that Apple stock was trading for about $500 per share. In Lesson #15, I taught you that you never want to put all of your eggs in one basket. Well, that was true, sort of…

ETFs allow you to bet as if you own the entire basket of eggs, even if in reality, you would only be able to invest in one egg. Said another way, ETFs magnify your ability to generate a posItive returns over the long-term.

Education:

In this lesson, we will get into some of the companies that offer the more popular ETFs that are available to investors like you. Since we learned that ETFs trade on stock exchanges just like stocks, there is a plethora of information to help you select the best investment option to fit your specific profile. The most popular ETF Rankings are in the following categories;

Large-Cap

Municipal Debt

China Region

Gold Oriented

Small-Cap

Corporate Debt

Emerging Markets

Commodities

Natural Resources

Real Estate

As you can surmise from the table, ETFs provide great investment flexibility. While you wouldn’t know which stock to invest in a Chinese company, a China Region ETF would enable you to invest in many Chinese companies all at once.

Remember that ETFs are best suited for long-term investors seeking low-cost, diversified portfolios.

Some of more popular ETFs are provided from the following firms who offer many options for investors.

Vanguard

Powershares

Ishares

SPDR (Spider)

MAGNIFY YOUR INVESTMENT RESULTS!

Resources:

SPDR University (http://spdru.com/) – SPDR University (SPDR U) provides online education built exclusively for investment professionals.

Important terms from this lesson:

Term

Definition

PowerShares

PowerShares is an investment boutique firm based near Chicago which manages a family of exchange-traded funds or ETFs marketed by Invesco.

IShares

iShares are a family of exchange-traded funds (ETFs) managed by BlackRock. Each iShares fund tracks a bond or stock market index.

SPDR

SPDR funds are a family of exchange-traded funds (ETFs) traded in the United States, Europe, and Asia-Pacific and managed by State Street Global Advisors (SSgA). Informally, they are also known as Spyders or Spiders.

Action Step: Let’s go back to college with SPDR University.

Go to SPDR University and view the online courses to learn more about ETFs.

You may know your ABCs, but do you know your ETFs?

The above image depicts a favorite dish from my youth, alphabet soup. Have you ever heard of S&P, NYSE, NASDAQ or FTSE? A better question may be, do you understand what these acronyms mean?

In the world of investing, it can often feel like you are in stuck in a bowl of alphabet soup. When most people see these titles, they are understandably intimidated. In this lesson, I will provide an introduction to Exchange-Traded Funds (ETFs) and discuss how they can be used to help you reach your investment goals.

Education:

The last category in the investing diagram is ETFs or Exchange Traded Funds.

An exchange-traded fund (ETF) is an investment fund traded on stock exchanges, much like stocks. An ETF holds assets such as stocks, commodities, or bonds. Most ETFs track an index, such as a stock index or bond index. The purpose of an ETF is to match a particular market index. Because, technically, you cannot actually invest in an index, exchange-traded funds allow investors to invest in securities which seek to replicate the index.

In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of the market. Indexes can be based on various categories of stocks. There are the widely known market indexes, such as the Dow Jones Industrial Average, the NASDAQ Composite, or the S&P 500. The Standard & Poor’s 500 (aka S&P 500) is one of the world’s best known indexes, and is the most commonly used benchmark for the stock market. The S&P 500 is a stock market index based on the market capitalizations of 500 large companies having common stock listed on the NYSE or NASDAQ.

When you buy shares of an ETF (e.g. Vanguard S&P 500), you are buying shares of a portfolio that tracks the yield and return of its native index, or the S&P 500 in this instance. Although the Vanguard fund was an example of overall stock market index, there are indexes based on market sectors, such as tech, healthcare, financial; foreign markets; market cap (micro-, small-, mid-, large-, and mega-cap); asset type (small growth, large growth, etc.); even commodities. ETFs provide great flexibility for niche investors.

Benefits of ETFs

ETFs combine the range of a diversified portfolio with the simplicity of trading a single stock.

Investors can purchase ETF shares on margin, short sell shares, or hold for the long term.

Passive management, fund or money manager makes only minor, periodic adjustments to keep the fund in line with its index.

ETFs mitigate the element of “managerial risk” that can make choosing the right fund difficult.

ETFs allows you to harness the power of the market itself.

Fewer administrative costs than actively managed portfolios.

Tax efficiency – fewer taxable distributions.

Highly efficient investment

Diversification

High liquidity – enabling investors to get into and out of investment positions with minimum risk and expense.

ETF shares trade exactly like stocks.

Resources:

CNN Money ETF Finder (http://bit.ly/1oTHzJH) – provides a tool to help investors find funds to fit their individual criteria.

The Vanguard S&P 500 fund – The Fund is a low cost way to gain diversified exposure to the U.S. equity market. The fund invests in 500 of the largest U.S. companies, which span many different industries and account for about three-fourths of the U.S. stock market’s value