In Lesson #10, we focused on the homeowner, but what about the people who are trying to decide if homeownership is for them? Personally, I believe that a home provides more wealth that can be enumerated; however, it is NOT required to be wealthy. There is no place where this is more truthful, than in New York City where many wealthy people still rent. If this sounds like a setup, then let me assure you that it is not. Buying a home may not be the best option for everyone and the truth is that it may ‘not’ save you money, it may ‘not’ be a factor for wealth creation, it may ‘not’ offer the best rate of return, and so on. It is important that you understand the cons of homeownership as much as the pros.

Education:

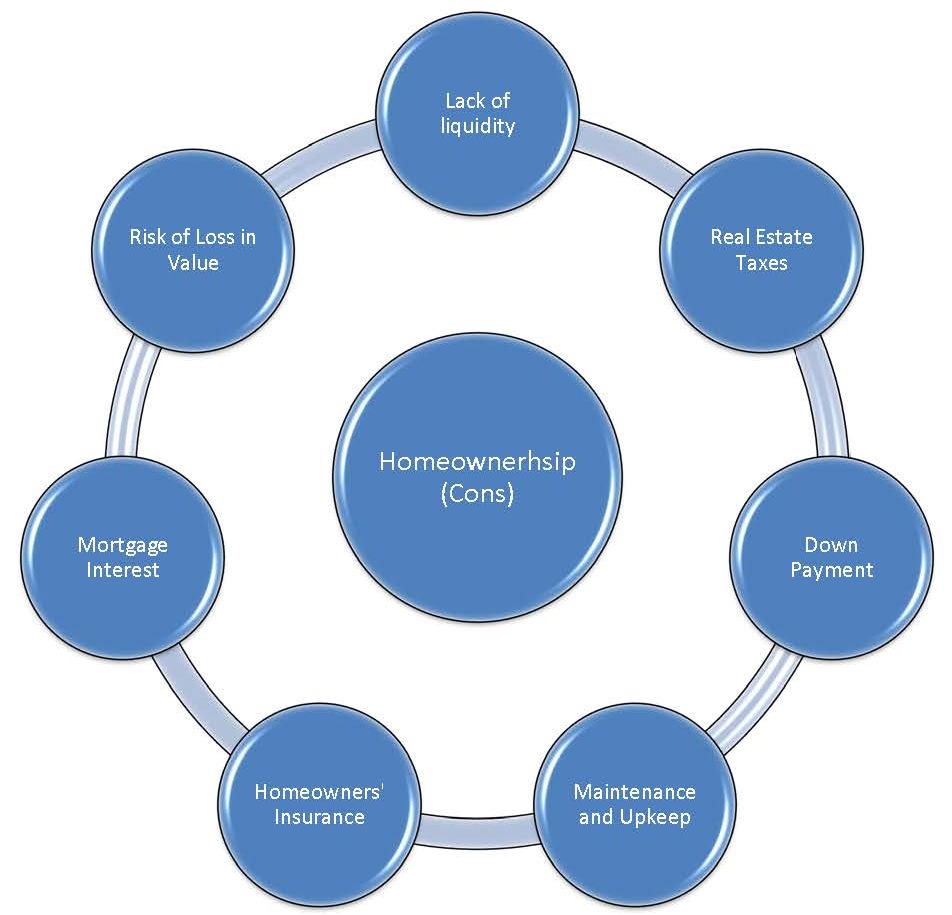

A house can be a wonderful thing and in the last two lessons, we discussed the upside (pros) of homeownership, but there is also a downside. The diagram below depicts some of the additional burdens that come with homeownership.

Hands down, the absolute best explanation that I have seen on this topic comes from Khan Academy. Please take a moment to view this video because Khan will totally change the way that you think about the rent versus buy conundrum.

Resources:

Khan Academy – Not-for-profit with the goal of changing education for the better by providing a free world-class education for anyone anywhere.

Important terms from this lesson:

Term

Definition

Lack of Liquidity

The inability to convert an asset to cash, if needed to take advantage of an alternative investment strategy or if cash is just needed.

After yesterday’s lesson, I received the following comment and question.

Comment: I know the depreciation due to the horrid market. That now investment property is a loss. Question: How do we mitigate the risk if our numbers are bad?

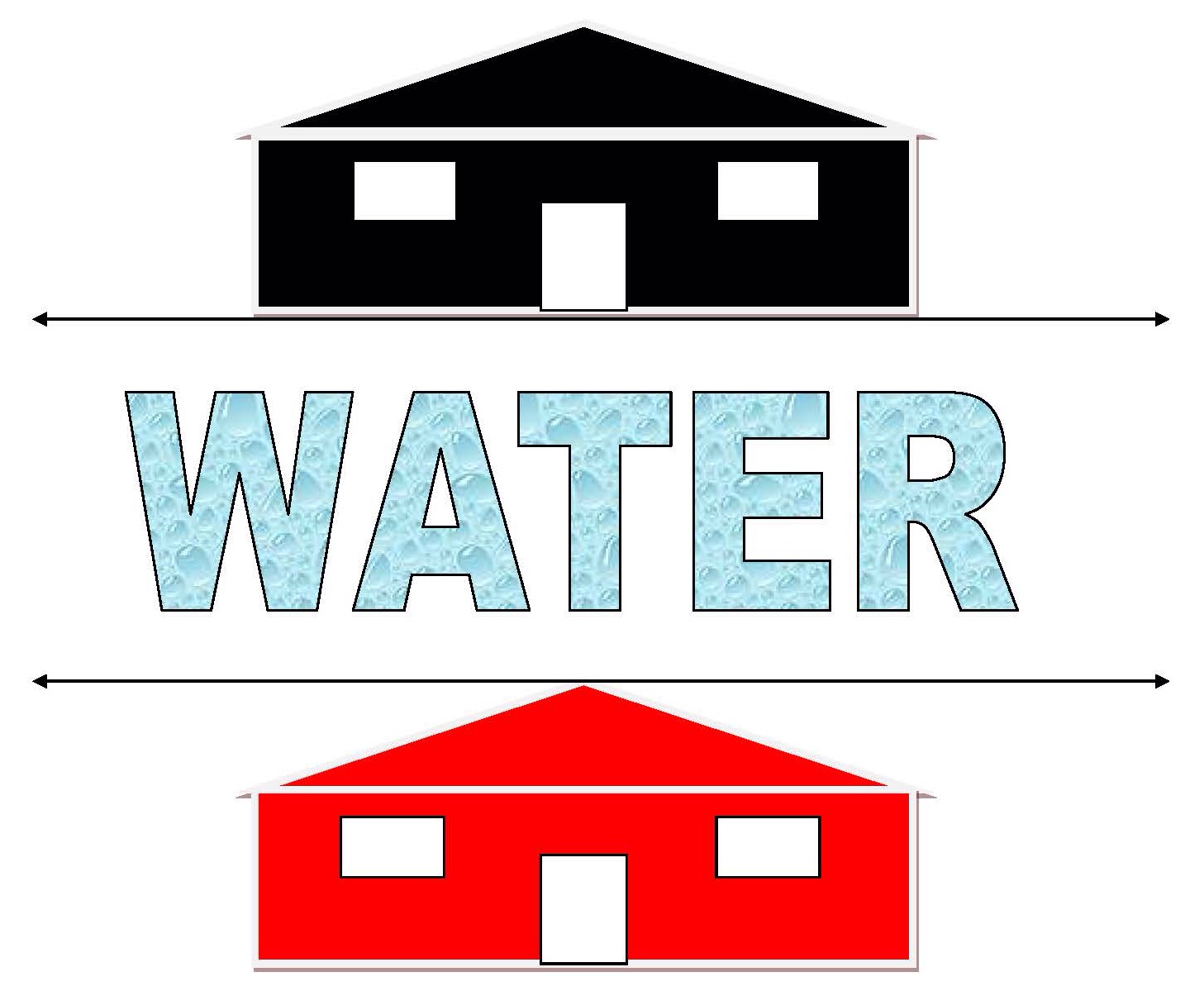

Are you Underwater?

The black house is a house of equity (possibilities), the red house is house of decisions (risk mitigation). In the black house, that is what we call ,“being in the black” and your equity gives you additional flexibility like “refinancing”. The red house is self-explanatory and although I love the color red, it’s never good when it comes to “being in the red” on your home.

Education:

Yesterday, we spoke about the equity and appreciation in your home, but after the housing crash of 2008, this may no longer apply to you. The truth is that the economic crisis left many homeowners “underwater”, a condition which results when the amount that you owe on your home (mortgage) is greater than the fair market value of your home. That is just a fancy way of saying that even if you sold your home, you would still owe money to the bank. What? Yes, you could give up your home and still owe money on it. What? Yes, it’s true, but there are ways to mitigate this if you understand the strategies available to you. Let’s call this the Underwater Mitigation Strategy (UMS). First let me say that this is nothing to be embarrassed about because this affected millions of homeowners, some who have had to make tough decisions. To determine the best UMS for you, let’s review the chart below.

Strategy

Pros

Cons

Tax Consequences

Stay and Hold

You keep the house (shelter) and wait to see if the value rebounds. An increase in value can restore your equity. This delays the UMS.

You may never recover your lost equity, you are paying for something which lacks value, refinancing usually is not available until equity is restored.

None

Loan Modification

The lender helps you stay in your home. Government offers programs to assist you like the Home Affordable Modification Program (HAMP)

Requires approval and the lender may not be willing to work with you.

None for now

Refinance

Same as Loan Modification

May not be a good option for homeowners with negative equity.

Sell or short sale (no bank approval)

Get rid of the cause of your stress.

You must find a new place to live; you still owe money to the bank (difference between what you received on the home and the mortgage); May trigger COD; Negative affect to your credit

COD Income MAY result in a tax bill in the worst possible time (income without cash)

Walk away (deed in lieu)

Get rid of the cause of your stress by giving the house back to the bank, but you walk away owing nothing else.

You must find a new place to live; Requires bank or lender approval which is hard to get; No real impact on credit

None

Foreclosure

You get to stay in the house during the foreclosure process.

You must find a new place to live; you still owe money to the bank (difference between what you received on the home and the mortgage); May trigger COD; Negative affect to your credit

COD Income MAY result in a tax bill in the worst possible time (income without cash)

Bankruptcy

You may be able to stay in your home. Gives you additional time to make a decision.

Won’t erase mortgage debt; may eliminate other debts which will allow you to afford your mortgage;

None for now

Resources:

Makinghomeafforable.gov – The Making Home Affordable Program (MHA) ® is a critical part of the Obama Administration’s broad strategy to help homeowners avoid foreclosure, stabilize the country’s housing market, and improve the nation’s economy.

Important terms from this lesson:

Term

Definition

Underwater Mortgage or Negative Equity

Mortgage balance exceeds the current market value of the loan.

Short Sale

Selling the home for less than then the mortgage balance.

Deed in Lieu

Strategy which allows you (upon approval) to simply give the home (deed) back to the lender and walk away fairly unscathed.

Cancellation of Debt (COD) Income

Phantom, but potentially taxable income which results when you sell the home for less than the mortgage. The difference between the mortgage balance and the amount received on the short sale OR for foreclosures, the entire unpaid mortgage.

Action Step: Find out if you are underwater.

Before you can address it, you must first diagnosis it. Pull up yesterday’s worksheet on Equity and Appreciation. Drop in your numbers to determine if you are underwater. If you are, then go through the UMS chart and determine which option or options may be best for you.

They all reference the asset that is the epitome and cornerstone of wealth building, the home. The three little pigs huffed and puffed about it, Dorothy clicked her heels to get back to it, Diana thought of home and so should you! A house is a magical thing because it has triple purpose. You can live in it, you can make money with it or you can use it to cease new opportunities in other areas of your life.

When you examine the net worth of wealthy individuals, they generally share one thing – they all own real estate or real property. There is that word again, OWN. Unless you live in New York, LA, San Francisco or some other city where home prices are ungodly, wealthy people do not rent because as we learned in the last lesson, your money should work while you sleep. What is a better illustration of money working while you sleep than in a house? A home can be a house, condominium, cooperative apartment (prevalent in urban areas like NY), or investment property. Speaking of wealthy people, here is a picture of the house Tyler Perry purchased for $7.6 million dollars that I add to inspire you.

A home falls into a category of assets called ‘real estate’, which is property consisting of lands, buildings, mineral rights, and the like. This lesson and the next will be dedicated to discussing this asset because you should either be a homeowner now or a future homeowner.

How do I make money with a house? I am glad you asked. Here is how.

Appreciation

Equity

Homes generally appreciate. That simply means that the value of the property increases while you live in it. To illustrate how appreciation works, if you purchase a house for $100,000 and then someone comes to you and offers to pay you $120,000 for your house, the difference is appreciation. In that case, you made a cool 20% profit simply from appreciation. That is new money or new wealth that you created. We will continue discussing real estate in Lesson #10.

Resources:

Zillow.com – Online real estate database.

Important terms from this lesson:

Term

Definition

Real Estate or Real Property

Property consisting of lands, buildings, mineral rights and the like.

Appreciation

The difference between your original purchase price and the fair market value of the home.

Equity

Your investment or ownership in the home. The portion that is not subject to mortgage…you own it outright.

Fair Market Value (FMV)

The price that you receive if you sold your home TODAY. The price that a willing, unrelated third party would pay creates its ‘fair’ market value.

Action Step: Dual assignment based on whether you already own a home.

For Home Owners – Figure out the amount of Equity and Appreciation in your home.

Equity = (Fair Market Value of Your Home Today – Your Mortgage Balance)

Appreciation = (Fair Market Value of Your Home Today – Your Original Purchase Price)

You should always know this. To find the fair market value, go to Zillow.com and type in your address. They will give you a little guidance about what your house would sell for today.

For Future Home Owners – Find a picture of a home and put it on your Vision Board. Then make a goal that you will purchase a home in ________ years.

Make you money get a job…make it work…while you sleep!

Did you know that a dollar a day could grow into a million dollars?

Now that I have your attention, I want to teach you to RESPECT YOUR DOLLARS!

In Matthew 25:14-30, Jesus teaches the timeless Parable of the Talents. You can and should read it for yourself, but it teaches the principal of being profitable and that no matter what you have, it can be increased if invested properly. Verse 25:27 in particular reads, “So you ought to have deposited my money with the bankers, and at my coming I would have received back my own with interest.” Wow, the bible never ceases to amaze me, but in this instance, Jesus was actually acting as a financial advisor by giving very sound advice. I will let the theologians analyze that, but I will take the lesson at face value.

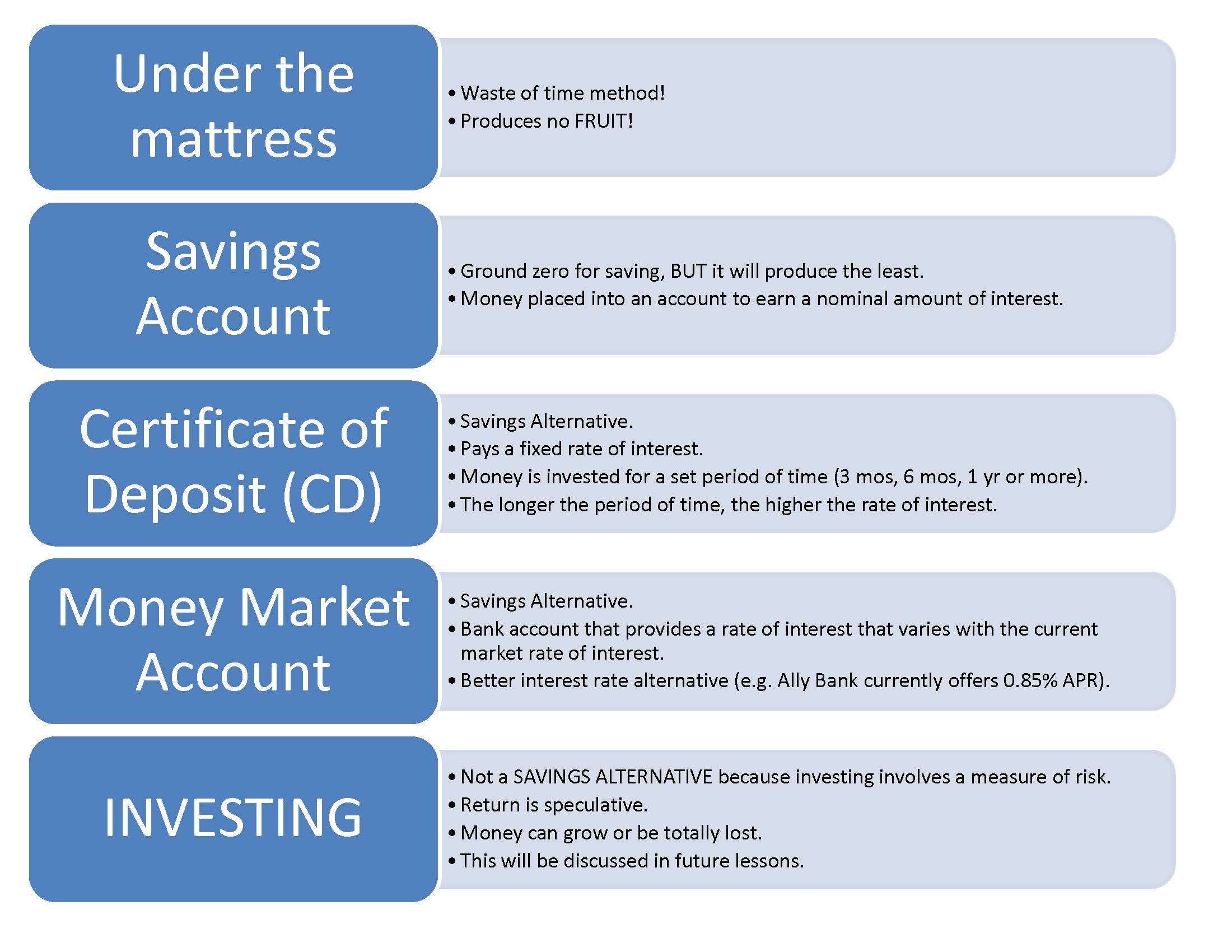

Now that you have diagnosed your financial health through your net worth, found a ripple through your cash flow budget and created a vision, you are ready to begin the real work. In this lesson, I would like to teach you about the different methods to save your money and earn INTEREST…that is putting your money to work.

First, think about money as a seed. If you hold the seed in your hand, then it will remain just a seed and/or die. However, if you plant or sow the seed, then the seed has the opportunity to grow and produce fruit. For financial purposes, WE WANT FRUIT! Fruit will enable you to reach your goals and live a life of financial freedom. Fruit creates more fruit!

Here are some Savings Alternatives that you may aid you to produce fruit.

Resources:

Bankrate.com – Great consumer finance website to compare financial products.

Ally.com – Offers competitive rates for its savings, CD and Money Market Accounts.

Important terms from this lesson:

Interest – Return on the use of your money

APR – Annual Percentage Rate is the rate that you will receive if your money is invested for a full annual period. For example, if you invest $1000 at a 1% APR, you would earn $10 annually on your investment.

Action Step: Pick a Savings Alternative for 2014.

Go to bankrate.com

Click the BANK ACCOUNTS tab.

Play with the menu options to see the different savings alternatives available to you.

“Vision without execution is hallucination.” – Thomas A. Edison

Yesterday, we kicked off Step One of our journey to create and develop assets. In the last lesson, I asked you to create your monthly cash flow budget. The budget is such a vital part of this process, so please continue working on that until you have an honest depiction of your monthly income and expenses. You cannot save or invest, if you don’t first find a ripple (refer to Lesson #6).

I found this quote in 2013 and it was an aha moment in my life. “Vision without execution is hallucination”, has become my personal mission statement. With that said, I would like to turn the quote around a bit and say, “execution without vision is a prelude to failure”. That was my wrinkle to the quote, but it is germane to our goal of ‘financial freedom’.

I want you to envision financial freedom and what that would look like in your life. I challenge you to document this vision on a VISION BOARD. Here is a picture of a vision board on Oprah.

Here is a copy of my Vision Board for 2014 that I’m working on. As you will see, it is not yet finished because this is my process. When I find items that line up with my vision, they go on the board. Remember the movie, Field of Dreams? Well, this is my canvas of dreams. a tangible reminder of my goals and when I sacrifice a moment of instant gratification, then I can go back to the board and be realigned by seeing my goals.

Important terms from this lesson:

1. Vision Board – Visual canvas depicting your goals.

Action Step: Create your VISION BOARD for 2014!

Go to a local store (CVS, Rite Aid, etc.) and purchase a poster board and either glue or tape. It doesn’t have to be fancy.

Think about why you are embarking on this journey. What are your goals?

Begin finding items, clippings, articles, affirmations, or anything that reminds you of your goal. Throughout 2014, I want you to add more and more things to the board. At the end of this process, I want to help you see a way to manifest these items in your life.

“You have to do something if you are going to get something.” TD Jakes

Ecclesiastes 7:12 “For wisdom is a defense as money is a defense, But the excellence of knowledge is that wisdom gives life to those who have it.”

Ecclesiastes 10:19 “A feast is made for laughter, and wine makes merry; But money answers everything.”

Money is provision.

Money is protection.

Money must be tied to purpose.

The first step to a life of wealth is the creation and development of assets. The first few lessons were to introduce and explain the concept of assets. To create something to OWN, we must assess what materials or resources are currently available to you. We began with net worth to enable you to diagnosis the current state of your wealth. Now it is time to roll up your sleeves and get to work. What resources do you have now? Do you know?

A cash flow statement can help you evaluate your personal income and expenses and see if you are running ‘in the red or the black’ each month. This will help you free up money to save or invest. A wave first begins with a ripple. In this lesson, let’s find the ripples.

Important terms from this lesson

1. Cash Flow Budget – An estimate of income and expenditure for a set period of time.

Action Step: Create your monthly cash flow (budget) statement.

Pull out your last three monthly bank and credit card statements. (This will help you pull the information to complete the cash flow statement)

“Whatever you can do, or dream you can, begin it; boldness has genius, power, and magic in it.” (Goethe)”

Saturday is a day of rest and reflection for many of us. Today, I encourage you to become a student of the lives and teachings of successful people. The only way to transform your financial life, is to do the work. A part of that work is finding your financial role model. Today’s lesson is to listen to a financial giant who teaches on wealth and success, Tony Robbins.

Important terms from this lesson:

1. Financial Freedom – Having enough wealth to live a life without limitations.

Action Step: Find a financial role model!

My financial role models are Oprah Winfrey and Sean “Diddy” Combs, two wealthy individuals who came from meager beginnings to build successful lives of wealth, influence and prestige.

Who is your financial role model? Learn about this person, follow them, read about them, hang a picture of them in your cubicle or office (okay, that’s a bit much), but you get the picture. Remember when Rocky was going to fight the Russian in Rocky IV (one of my favorite movies)? Well, he hung a picture of him on his mirror as his daily reminder of his goal. Once you decide on your financial role model, make them a focal point of motivation.

Income inequality is a false precept! I know the politicians, namely the Democrats, pontificate about “income inequality” in an effort to arouse the electorate, but check this out.

“At least 268 of the 534 current members of Congress had an average net worth of $1 million or more in 2012, which amounts to just over half. The congressional median net worth was $1,008,767.”

The top 10 richest members of Congress; Average Net Worth (rounded to the nearest million):

1. Darrell Issa (R-Calif); $464 million

2. Mark Warner (D-Va.); $257 million

3. Jared Polis (D-Colo.); $198 million

4. John K. Delaney (D-Md.); $155 million

5. Michael McCaul (R-Texas); $143 million

6. Scott Peters (D-Calif.); $112 million

7. Richard Blumenthal (D-Conn.); $103 million

8. Jay Rockefeller (D-W.Va.); $101 million

9. Vernon Buchanan (R-Fla.); $89 million

10. Nancy Pelosi (D-Calif.); $88 million

(Note: Taken from Slate.com article entitled “Most Members of Congress are Millionaires” by Katie Long)

So don’t be fooled! The reason that income inequality is a false precept is that there is no equality in sacrifice or effort. If you bust your hump, sacrifice instant gratification in pursuit of your goal and your income increases because of that, should someone who did not do those things have an income equal to yours? Certainly not!

Income inequality should be rephrased to “Opportunity Inequality”. That gap can be closed through education and information. So instead of politicians advocating against wealthy people, they should work to promote “Opportunity Equality” or teach us how they created their wealth.

Did you know that there are 85 people who are as wealthy as half the WORLD? If you don’t believe, read for yourself at http://huff.to/1dUFcD4. But I say, DON’T HATE…EMULATE! The reason that these individuals are wealthy is because they are ASSET RICH…remember that term from Lesson #1? Instead of envying them, we need to follow their model. Many of them achieved wealth through business, some through real estate, some through investments, and some were beneficiaries of a prior generation. You know what makes them different from you? NOTHING!

The first three lessons were dedicated to driving home this simple formula (Assets – Liabilities = Net Worth). It is the same, exact formula that businesses use to determine their value. And why not use this?…YOU ARE THE CEO OF YOUR FAMILY! Think about that for a moment. I bet you didn’t realize that, did you? In the days to come, I will teach you how to put together your own personal financial statements. But this lesson is to gauge your understanding of this formula. Your net worth can be either “positive” or “negative”. So what is yours?

Important terms from this lesson:

Positive Net Worth – Your ASSETS are greater than your LIABILITIES.

Negative Net Worth – Your LIABILITIES are greater than your ASSETS.

Income inequality – The false precept that suggests that income should be equal.

Opportunity inequality – The precept that suggests that opportunities are unequal.

Action Step: What is your NET WORTH?

Please print out and complete the Net Worth Worksheet. Short worksheet with 4 short steps.

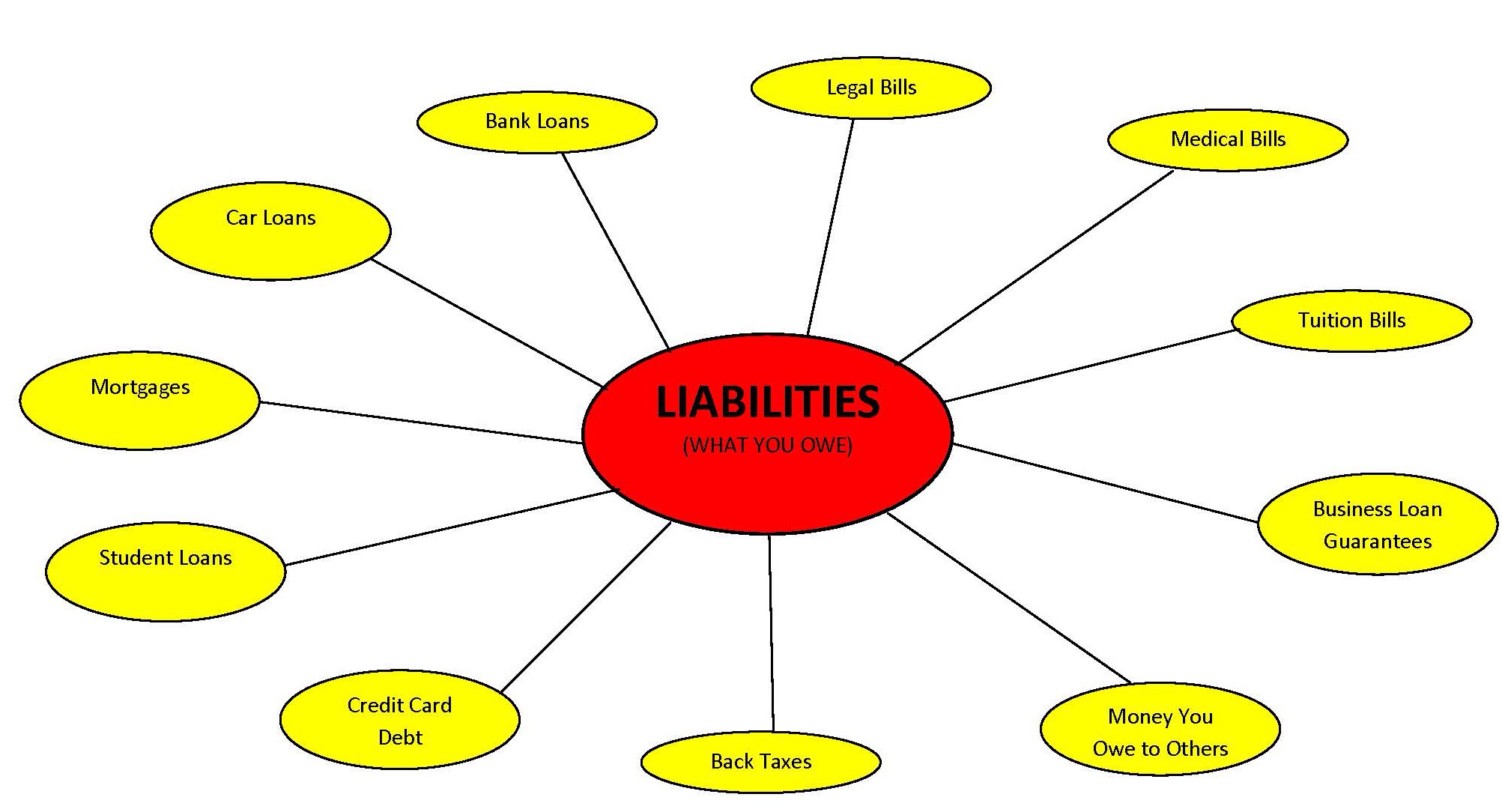

In the first two lessons, we concentrated on the concept of assets and what you OWN, however, that is only one side of the coin and I would say the “positive” side. But, for every ‘ying’, there is also a ‘yang’…the flip or “negative” side of the coin. In this lesson, the flip side of the coin is called LIABILITIES. This concept is more prevalent and dare I say, more important than knowing your assets, because LIABILITIES are what you OWE!

Let’s think about Michael Jackson before his untimely death (R.I.P. King of of Pop). Well, Michael Jackson had a great deal of assets…remember the ferris wheel at Neverland? The white glove? Ironically, which is currently hanging in the Mandalay Bay Hotel in Las Vegas Although he had a plethora of assets, the man in the mirror actually OWED more than the value of those assets. That put him in a hole, which I still believe was the impetus for his early death. So, let’s take a deeper look at your LIABILITIES.

In laymen’s terms, an LIABILITY is something that you “OWE”! That’s it…you OWE some person, business or entity (a debt). You are in the hole! Several years ago, a friend of mine named Cliff Goins IV wrote a book entitled, Stop Digging!: A Spiritual Guide to Financial Freedom and Sound Stewardship, that you can still purchase on amazon.com (http://amzn.to/1iqIfov) I always loved that title because you cannot realize wealth until you did yourself out of the hole.

Some examples of LIABILITIES for individuals are:

Important terms from this lesson:

Liabilities – Something that you OWE.

Debt – The total value of your liabilities (how deep the hole is).

Action Step: What LIABILITIES do you OWE?

Please print and complete the Liabilities Inventory Worksheet. This may take a little effort, but force yourself to jot down every single item that you OWE and take a real inventory of the size of the hole that we have to dig from! You absolutely need to understand what you OWE to determine how much digging will you need!

Click the link to download the Liabilities Inventory Worksheet – http://bit.ly/1iskbBV

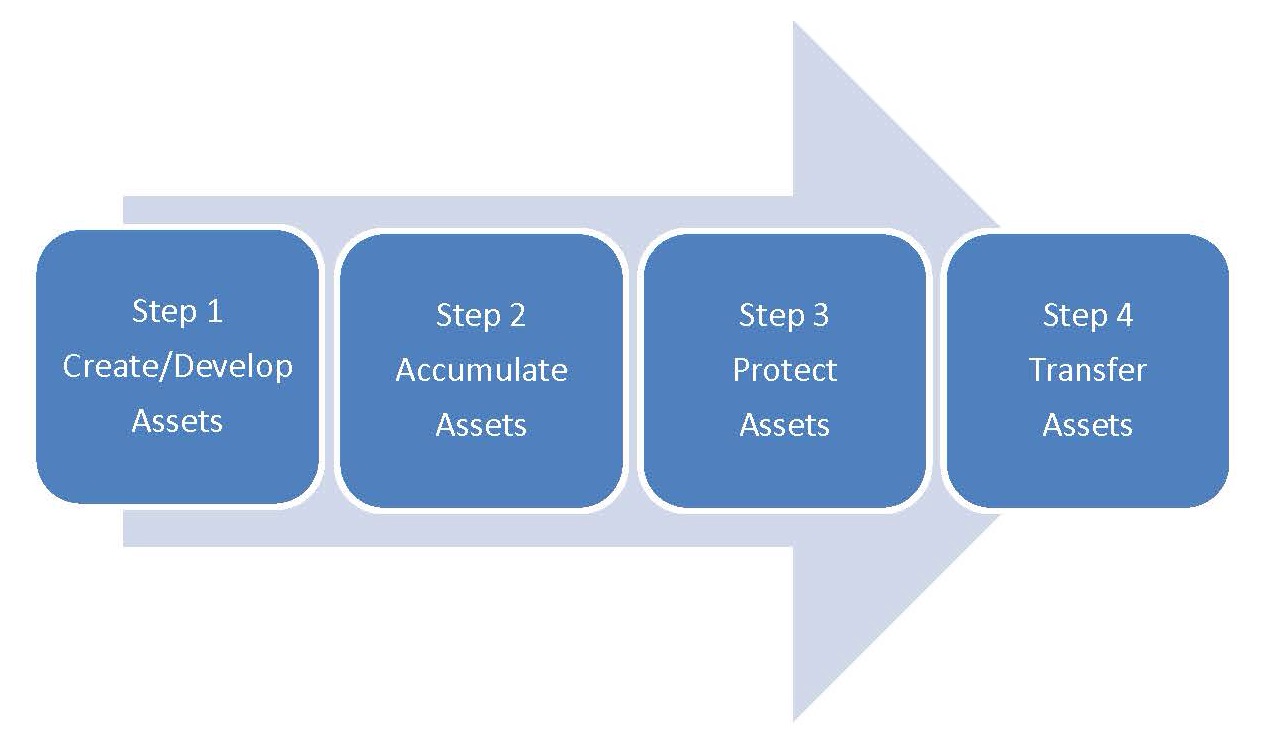

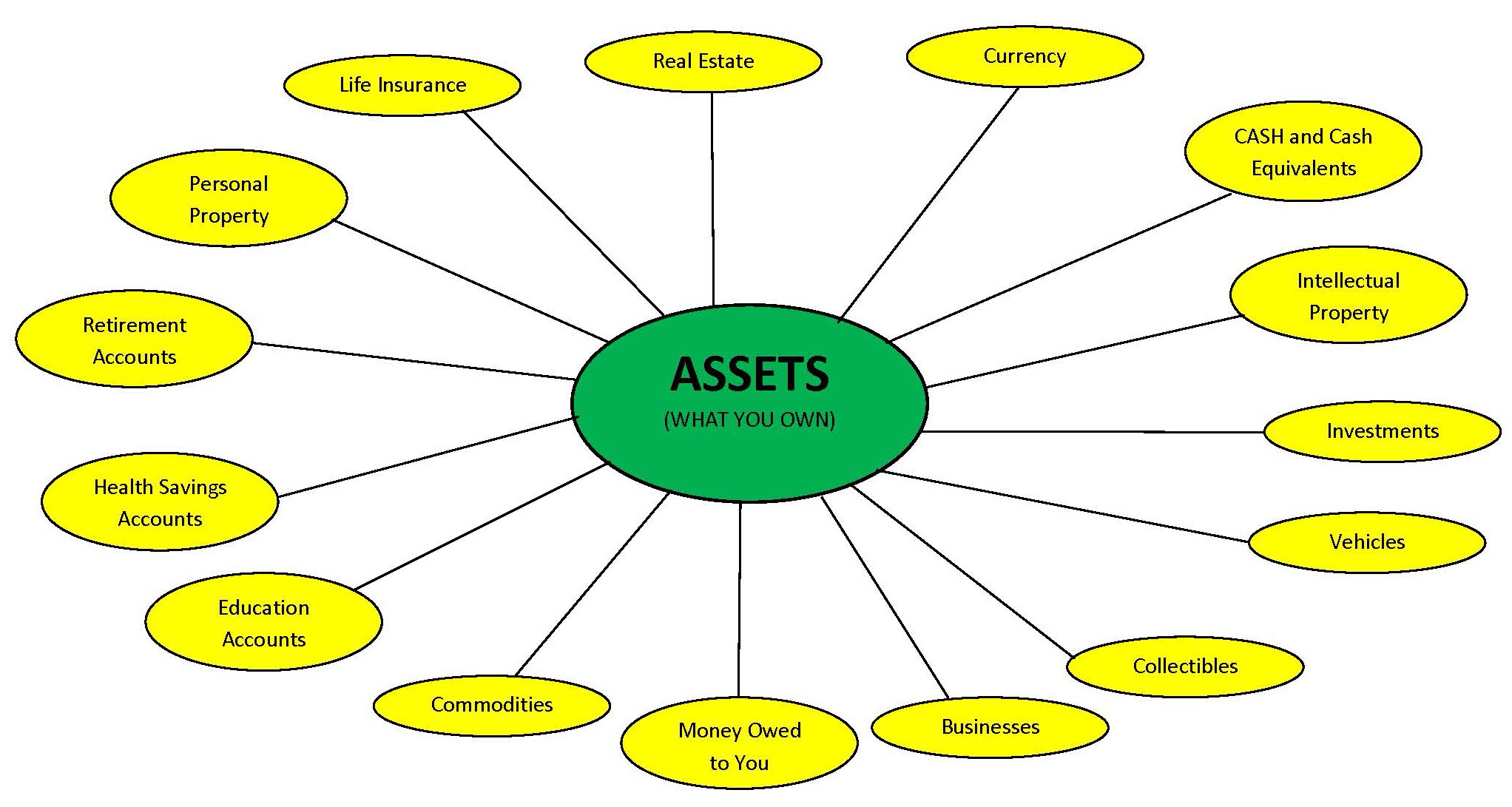

In Lesson #1, the goal was to introduce a very important (critical) concept to the discussion of wealth, ASSET. As important and critical as it may be, many people have no reference for what this simple five-letter word means. Assets are quite simply, the building blocks of wealth! Without assets, wealth just does not exist much in the same that you cannot build a mansion without a solid foundation. Then how can something so important and critical to the understanding of wealth be foreign to so many people? The answer is that we live in a SPENDING society of super Consumerism (my new term). The people who sell goods are often ASSET, while many of our super Consumers are ASSET POOR. It comes down to understanding your assets, namely how they are created, accumulated, protected and the transferred to future generations. What do the following families have in common?

Dynasties are families who create ASSETS >>> accumulate ASSETS >>> protect ASSETS >>> transfer those ASSETS to future generations. That is it! There is nothing special or unique about them. It is something that everyone…all of us can do! Let’s look at the journey of ASSETS through this illustration.

In Lesson #1, I asked you to complete the Asset Inventory Worksheet. It’s okay if you have not finished, but I want you to begin thinking about everything that you have. For my visual learners, go through each bubble, and check off what you currently OWN. So, do you have any ASSETS?

Important terms from this lesson:

Asset Rich – The abundance of ASSETS.

Asset Poor – The absence of ASSETS.

Dynasties – Families who create, accumulate, protect and transfer ASSETS to future generations.

Action Step: Let’s Create some ASSETS!

The easiest asset to create is cash because most of us have at least $1! The cash in your pocket or pocketbook is sitting in the chamber ready to be fired at the next purchase. Instead of doing that, I want to challenge you to look at that cash as your opportunity to CREATE AN ASSET. Many of you have heard about the 52 week money challenge. I actually did this in 2013 along with some colleagues. On 1/3/14, I took that money to my financial adviser at Edward Jones and we put that cash into a Bond Fund (Investments Category). I will explain what that means in a future lesson. It’s that easy, I took something that was lying around ready to be spent and created an asset. I’m doing it again for 2014, but instead of holding it and then taking it to my adviser, I have set up a money market fund and each week, I transfer that week’s contribution to the fund. Now, my money is making money (interest – to be explained in the future).

I want you to take the 52 week money challenge for yourself and each of your children.

For you, follow the program without deviating. At the end of the year, you will have CREATED A CASH ASSET worth $1,378.

For your children, divide the normal 52 week challenge by the number of children that you have.

For example, if you have two children, the contribution for Week 1 is $1. You would split that so that each child has $.50 saved for Week 1.

Repeat this every week following the chart. At the end of the first month, you will open up a money market account for yourself and your children. Don’t worry, I will teach you about Money Market Funds and advise you about how to select the best option for you and your family.

Click the link to download the 52 Week Money Challenge Worksheet – http://bit.ly/1edTVUz